Power Semi Small Caps

3 small caps that have the best Risk/Return and haven't gone parabolic yet

Disclaimer: This is not FA and I own some positions in the stocks mentioned. Very risky stuff and most people should stay away

—————————————————————————————————————————————————————

A few months ago, I talked about Status quo and the fundamental shift that is required to realize 30-50X increase in Power density within AI data centres.

Let me do a quick recap

Problem:

• A single NVIDIA B200 or AMD MI300X consumes 0.9kW – 1.4 kW. Dont even ask me about Ruben.

• A “pod” of 8 such accelerators + CPUs approaches 12–15 kW

• An AI training cluster is hundreds of pods – multi-megawatt

At 12 V distribution you would need kilo-ampere bus-bars thicker than a wrist; power loss alone would exceed the chips’ TDP

• On top, Every 1 cm² of copper busbar you delete saves you north of $20/kg and a small argument with the procurement team.

Hear about it directly from the Horse’s mouth

NVIDIA’s own whitepaper claims ~45% less copper in an 800 V plant.

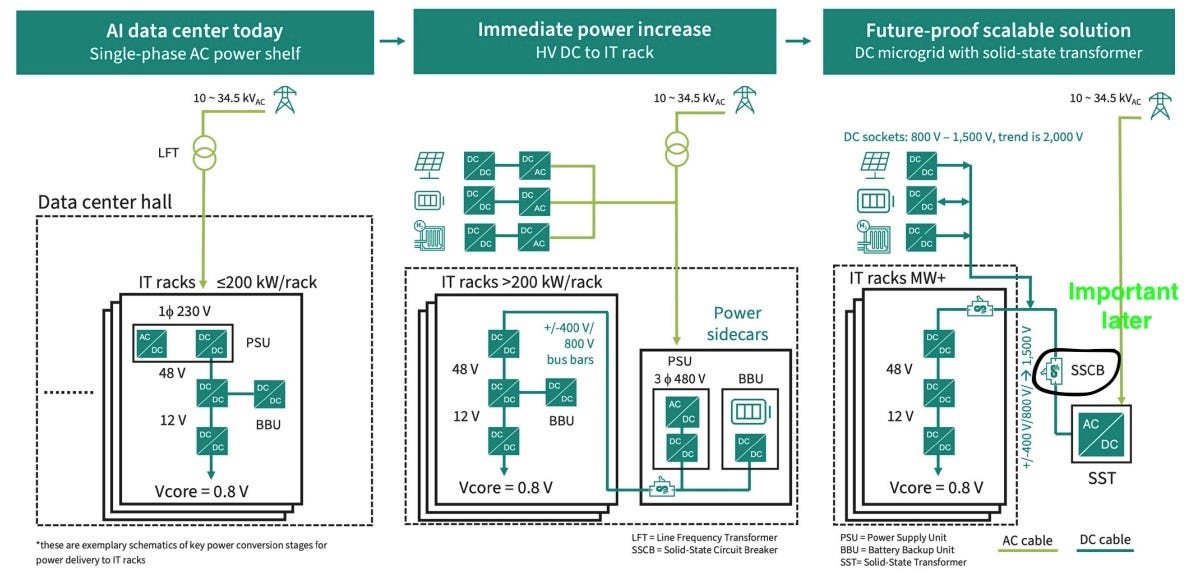

So First principles first, whats actually happening?

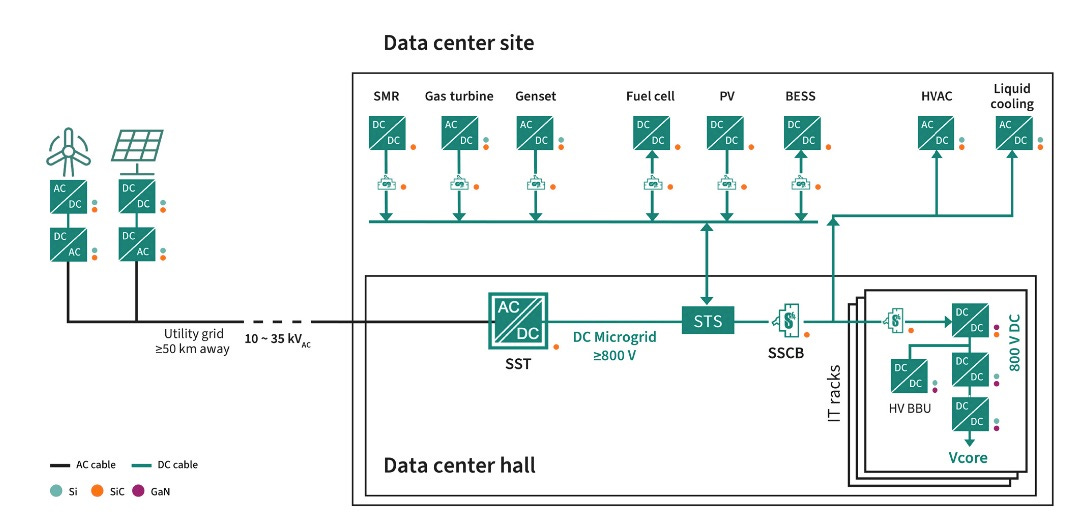

Here is a nice infographics to follow along the transition. Power distribution is changing from AC into DC microgrids.

Optics is forcing this transition quickly. And now that the retail knows what happened to Optics stocks, they are coming swinging for this sector too.

Here is what you need to understand about the Power Semis

Voltage is the cheat code. Crank it up early and keep it up for as long as possible. Then step it down ONLY inches from silicon, and you can unlock power dense, greener, cheaper AI factories.

If you need a refresher, go read this 6 months old post first.

On this post, VICR did 5X since this post.

If you are confused about SiC, vs GaN etc. Here is a great infographics that shows where does each of them thrive in the Data center value chain

Now that the market is interested in this deeply, lets go through the 3 small cap names that might do a few multi baggers for us. I will assess them and rank them.

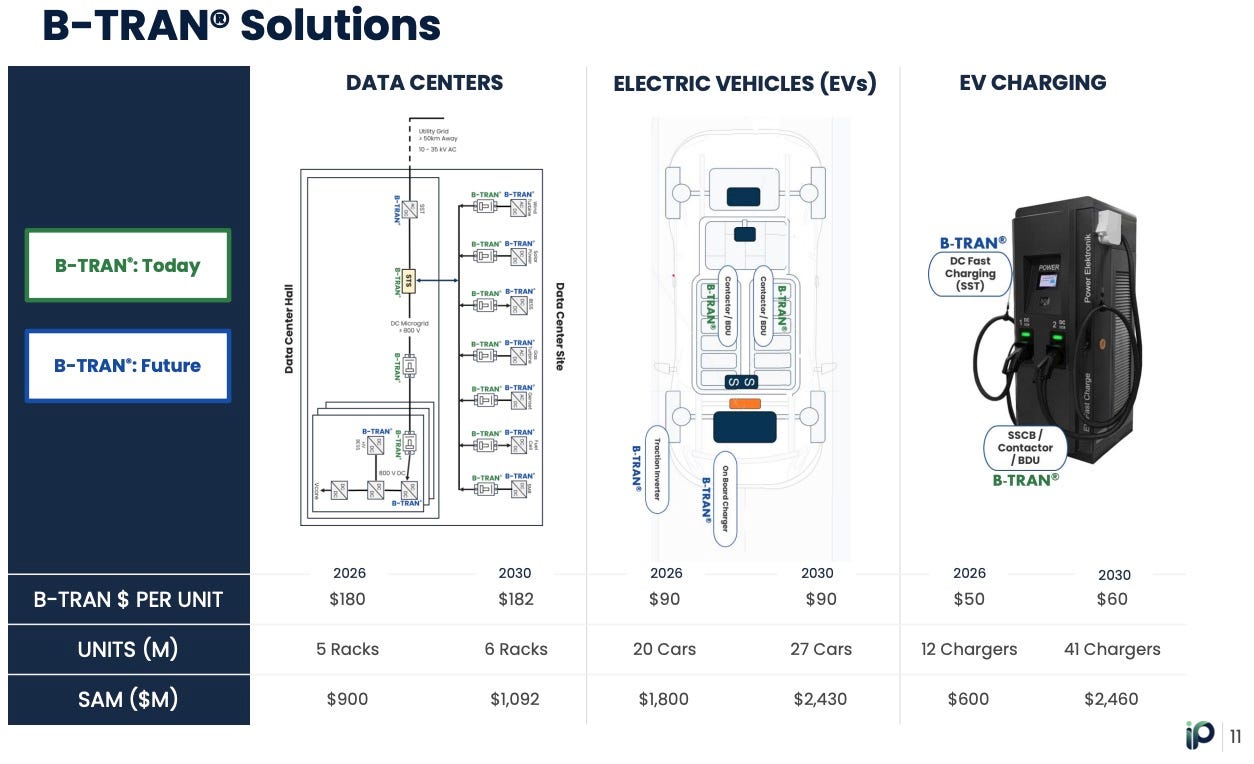

IPWR: ($45M MC. Riskiest with the highest upside )

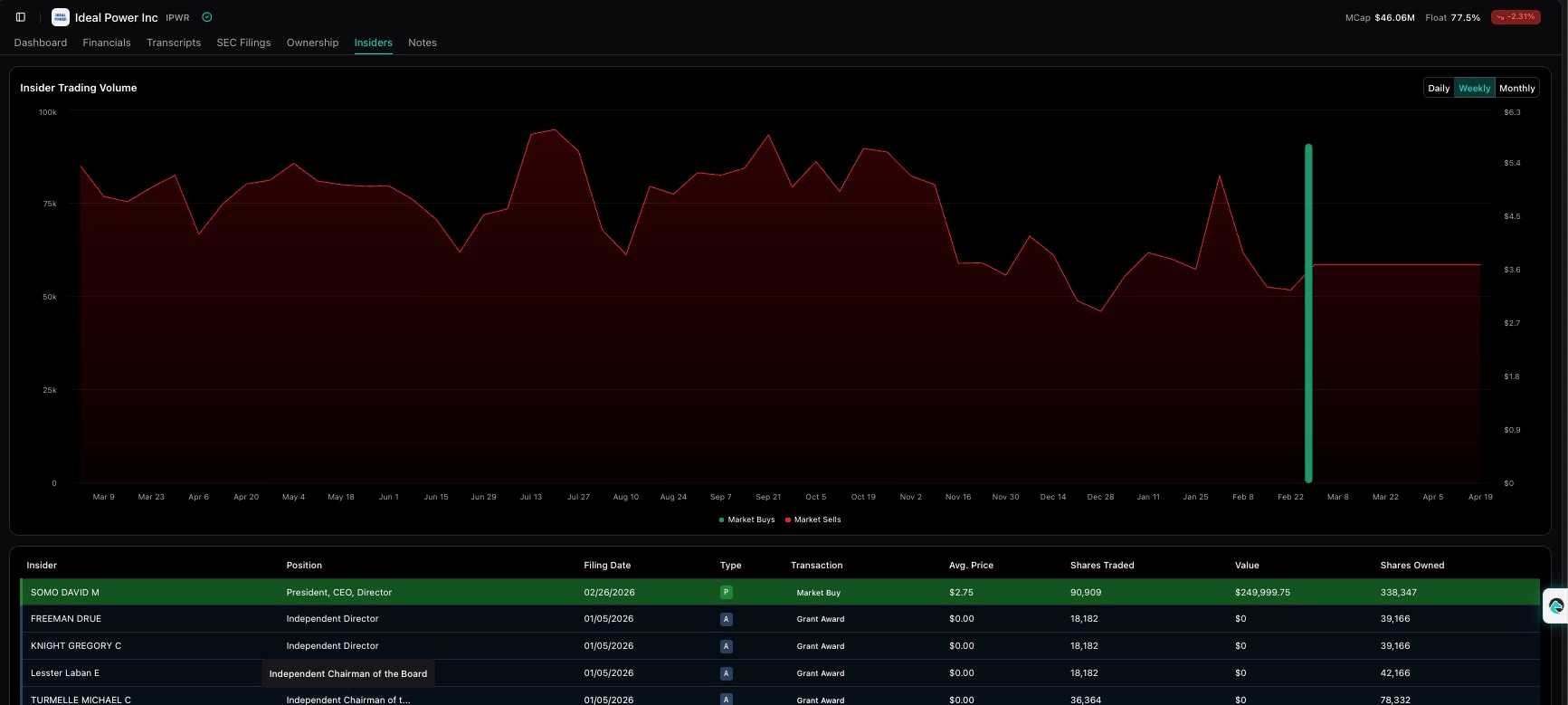

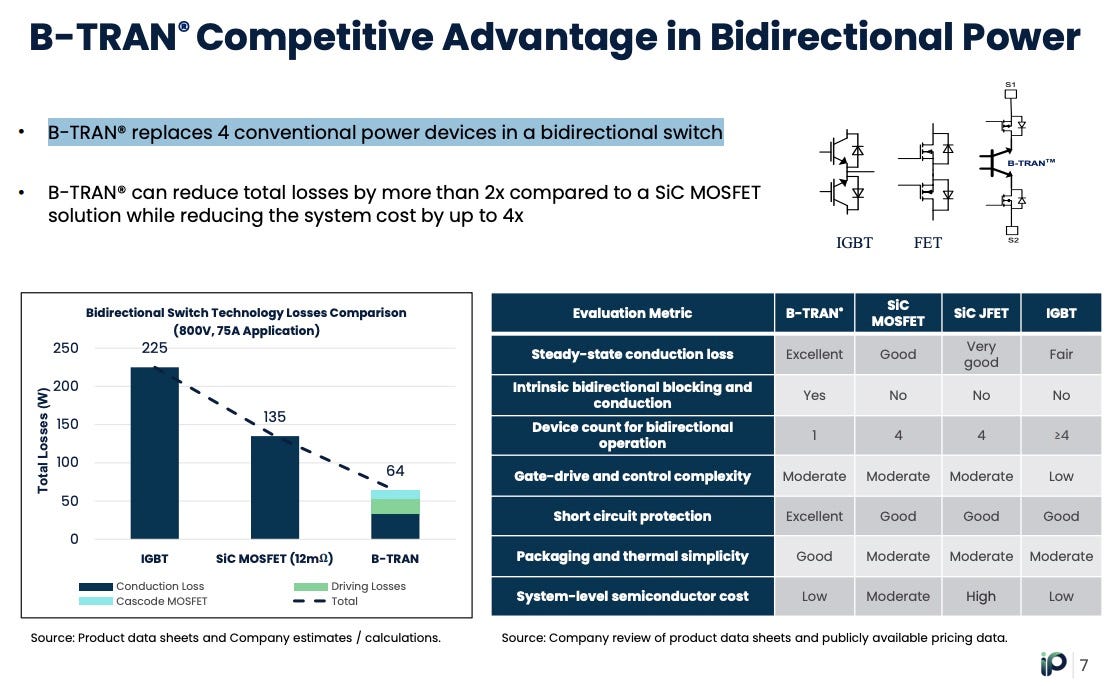

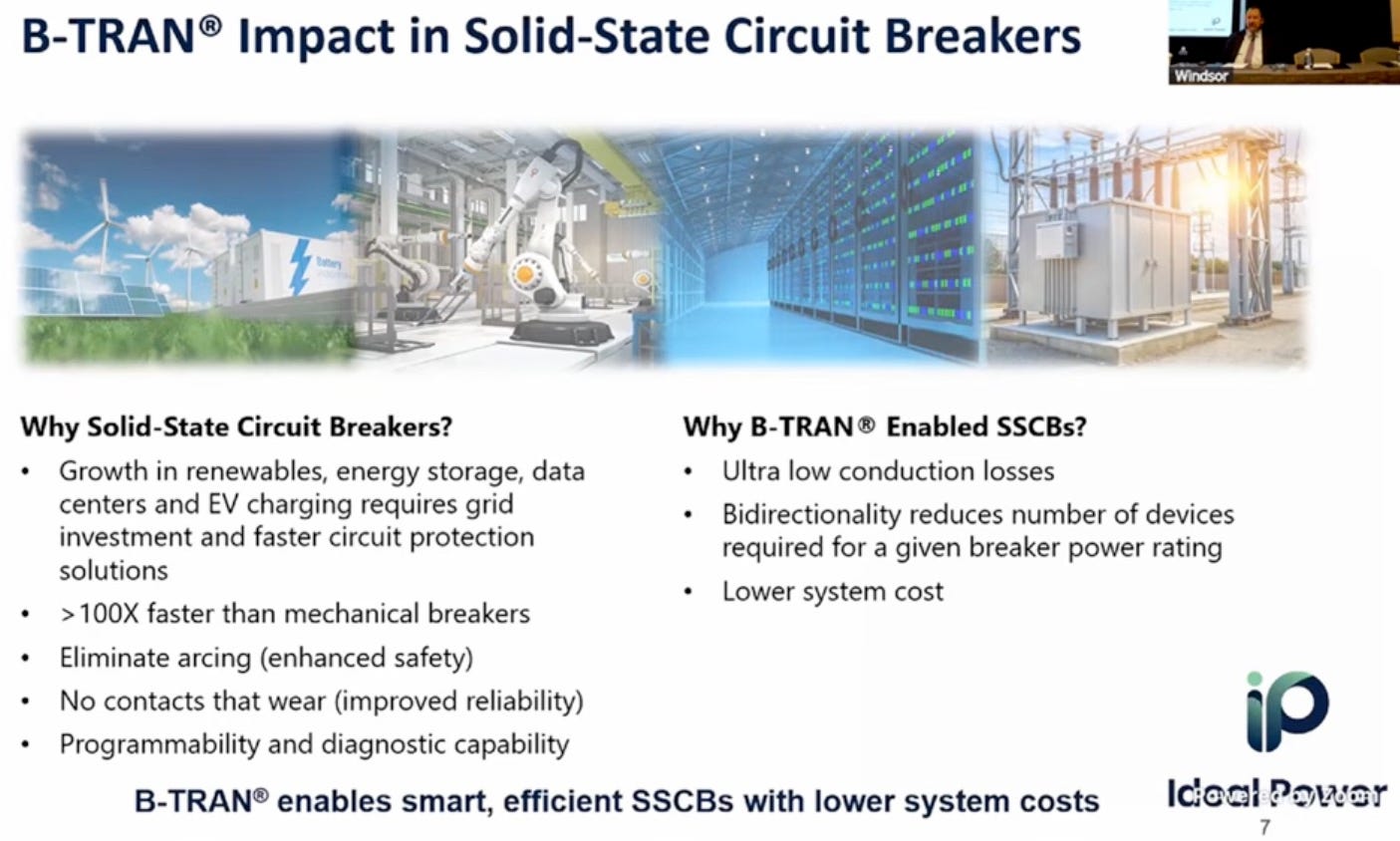

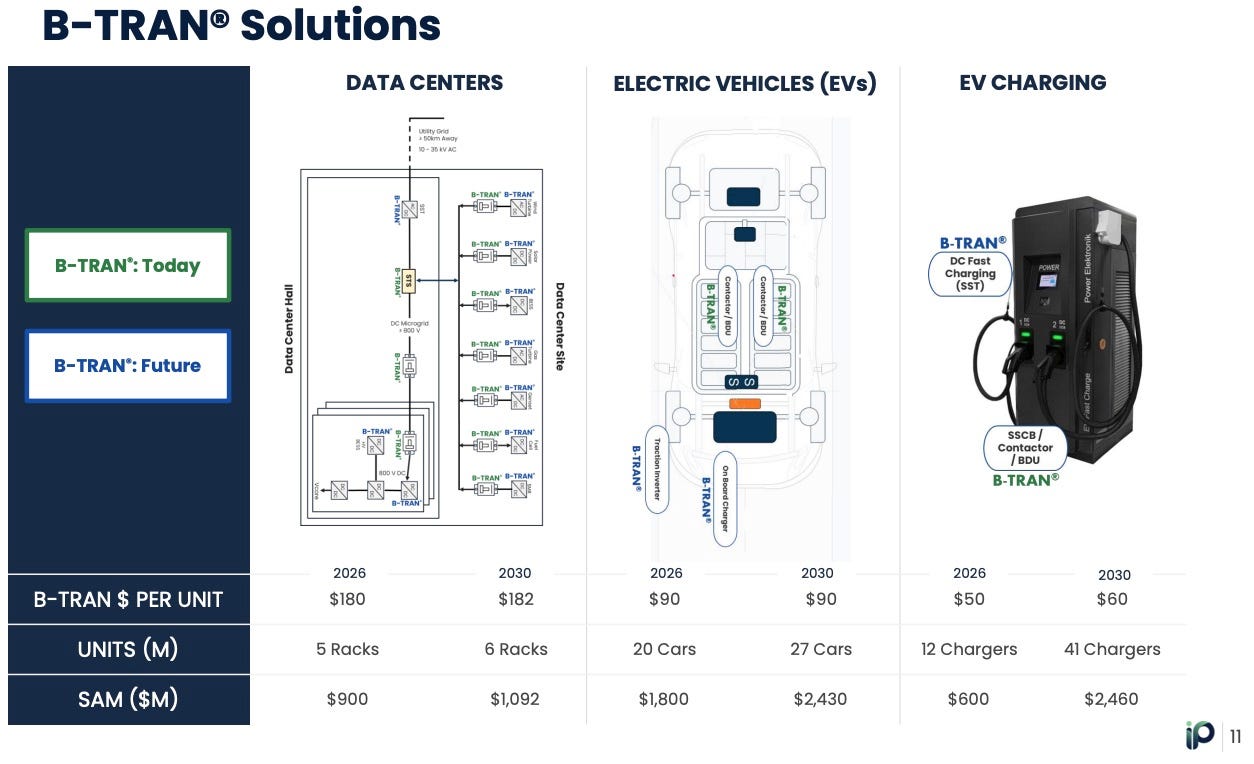

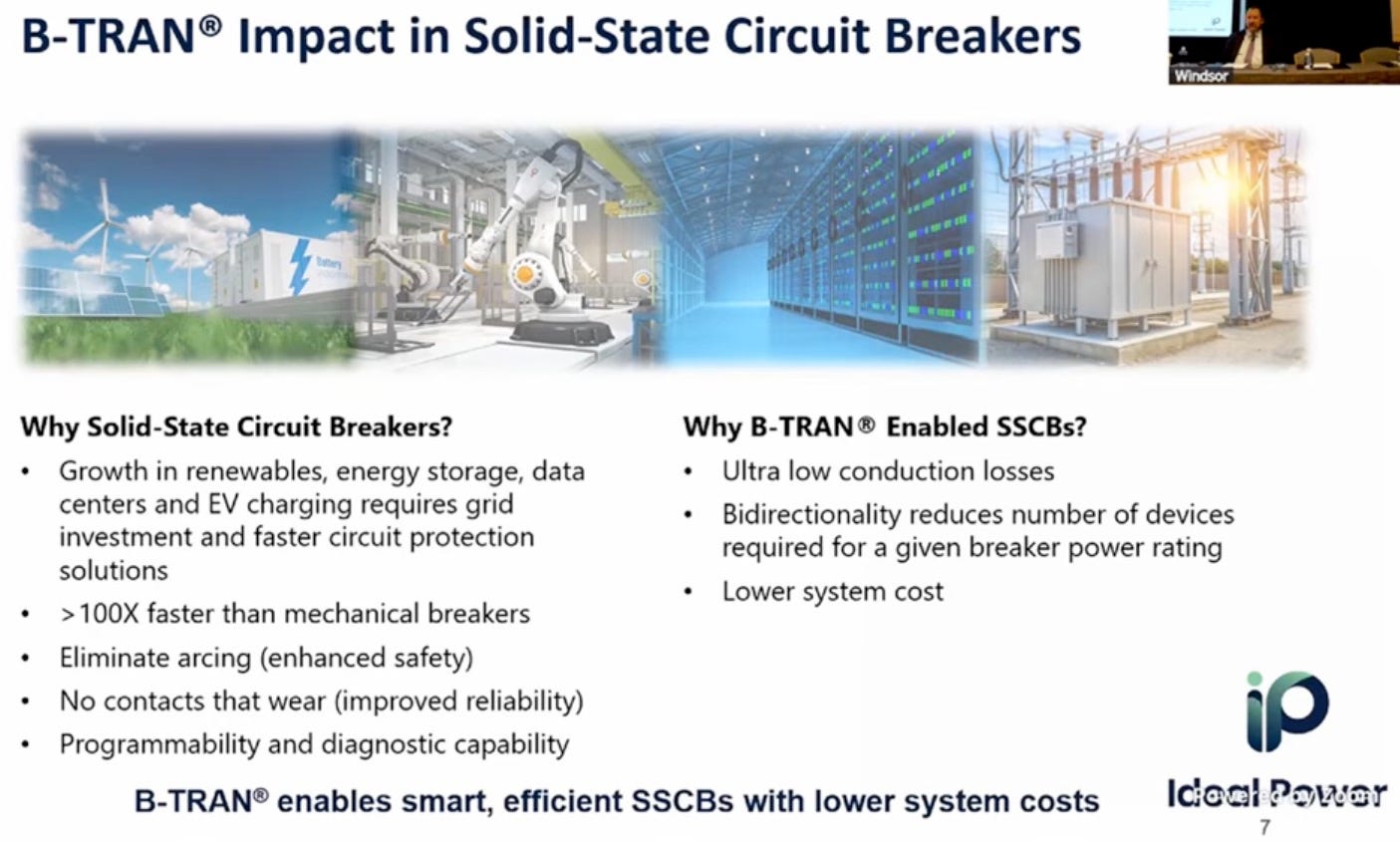

The 800V DC data center transition is creating structural NEW demand for solid-state circuit breakers. B-TRAN is uniquely positioned to serve this. CEO bought $250K personally at $2.75 (the 52-week low).

- Lead customer qualification Q4 2026, revenue ramp 2027. Markets might sniff it out if it works. They are eyeing the $200M sales pipeline

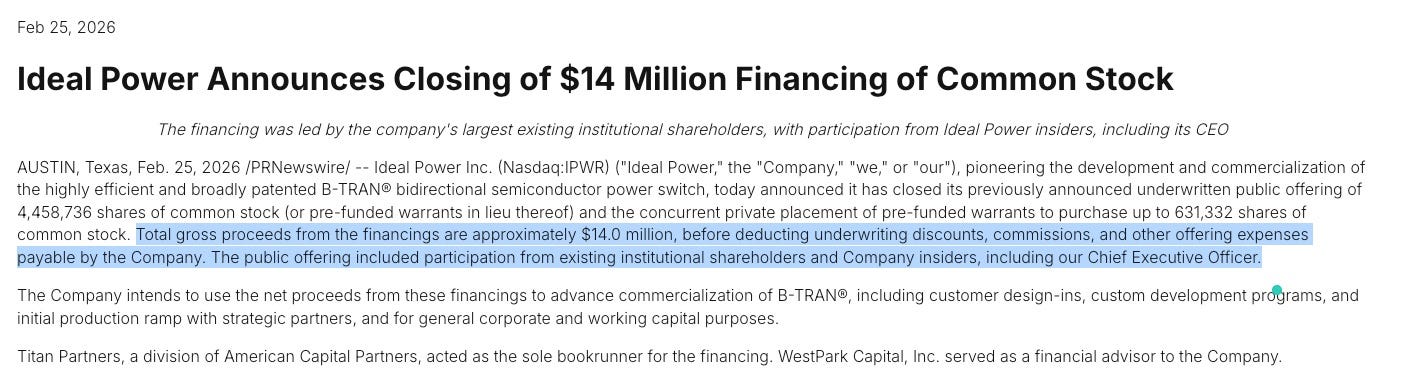

- They raised recently and will enough cash until the end of year atleast.

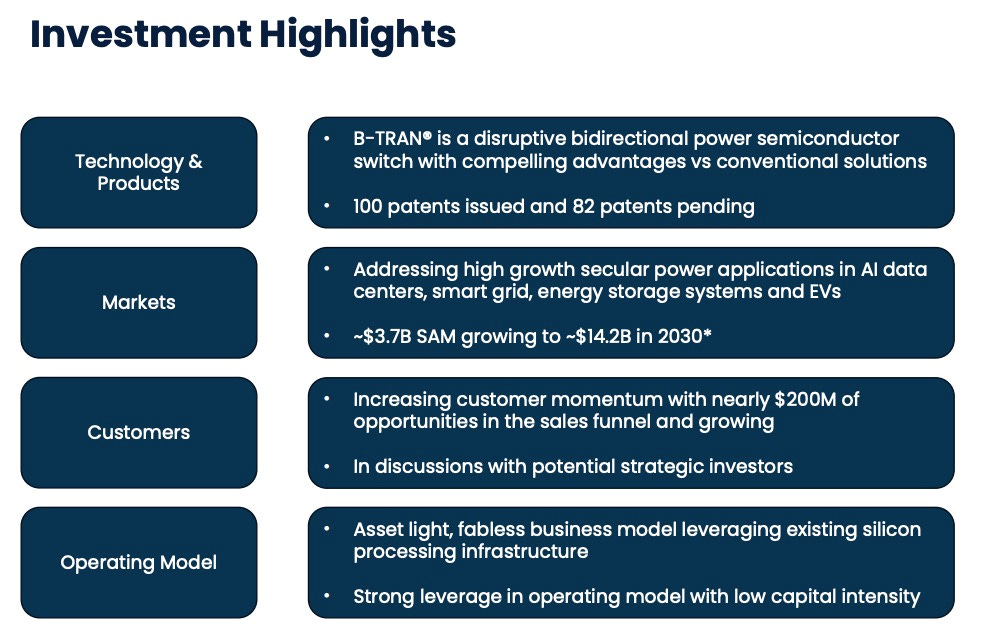

All excellent points from their deck

Under‑Appreciated Technical & Strategic Angles

IPWR’s B‑TRAN architecture targets a part of power semis that many investors (and some comps like NVTS) barely touch.

B‑TRAN is a fundamentally different device: a true bidirectional bipolar transistor vs. unidirectional FETs and IGBTs.

B‑TRAN: one double‑sided device replaces four devices (two switches + two diodes) in a conventional bidirectional leg.

Economic value is in bidirectional, high‑current protection and switching, not just generic conversion (where NVTS focuses).

Design‑win path and Stellantis work suggest “system‑level” attach, with long product lives once designed in.

Capital‑light model with foundry partners lets them scale on mainstream silicon, not exotic substrates.

Patents: 52 U.S. + 47 foreign issued, 76 pending (as of 12/31/2025) on B‑TRAN.

NVTS’s GaN is optimized for high‑frequency switching DC‑DC and AC‑DC; in protector/contactor/SSCB roles its conduction losses and need for extra devices are typically worse. Module‑level density and thermals

Fewer die + much lower conduction loss ⇒: Smaller heat sinks and bus bars.

Implication vs NVTS:

Navitas competes mainly in conversion (chargers, inverters, some motor drives) with unidirectional FETs; IPWR is attacking bidirectional protection and switching functions where a true bidirectional bipolar device has a structural advantage and can displace multi‑device SiC / IGBT stacks.

NVTS has a strong GaN IP portfolio, but it’s all FET‑based. To attack IPWR head‑on in these exact bidirectional switch topologies, they’d likely need new IP and process development.

Key Disconnect and Summary

Binary pre-revenue bet, but the risk/reward is massively asymmetric. Lead customer qualification Q4 2026, revenue ramp 2027. Markets might sniff it out

Risk: Pre-revenue. Illiquid. Technology adoption could slip. If B-TRAN doesn’t get qualified by year-end, cash runway becomes a concern.

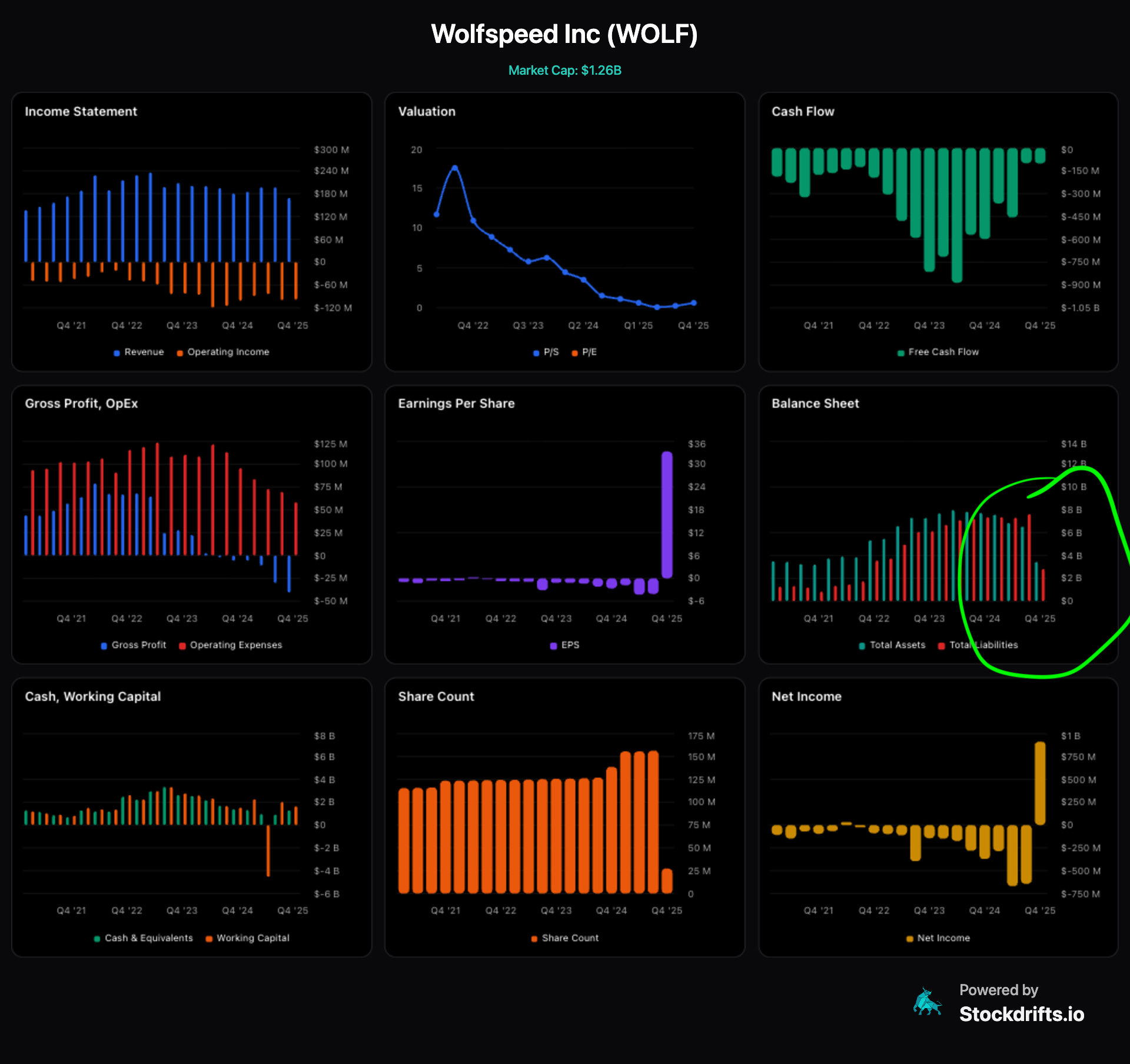

WOLF: ($1.26B)

SiC is becoming the bottleneck material for the AI power stack. Structural capacity constraint on Silicon Carbide wafers. Wolfspeed owns the only 200mm wafer fab on the planet. They are lining up for 300mm wafers and do it in Ameria. Supply chain risk might make this a strategic priority

The Alpha: Market cap (~$1.25B) roughly equals cash ($1.3B). You’re getting the world’s only 200mm SiC fab, 2,300+ patents, and 300mm SiC technology leadership essentially for free. Renesas’s $2B+ investment implies $55-65/share — nearly 2x current price. AI data center revenue is growing +50% QoQ.

Analysts still have a consensus “Reduce” at $14.33 target — 48% below current price. They are stale and will be forced to upgrade.

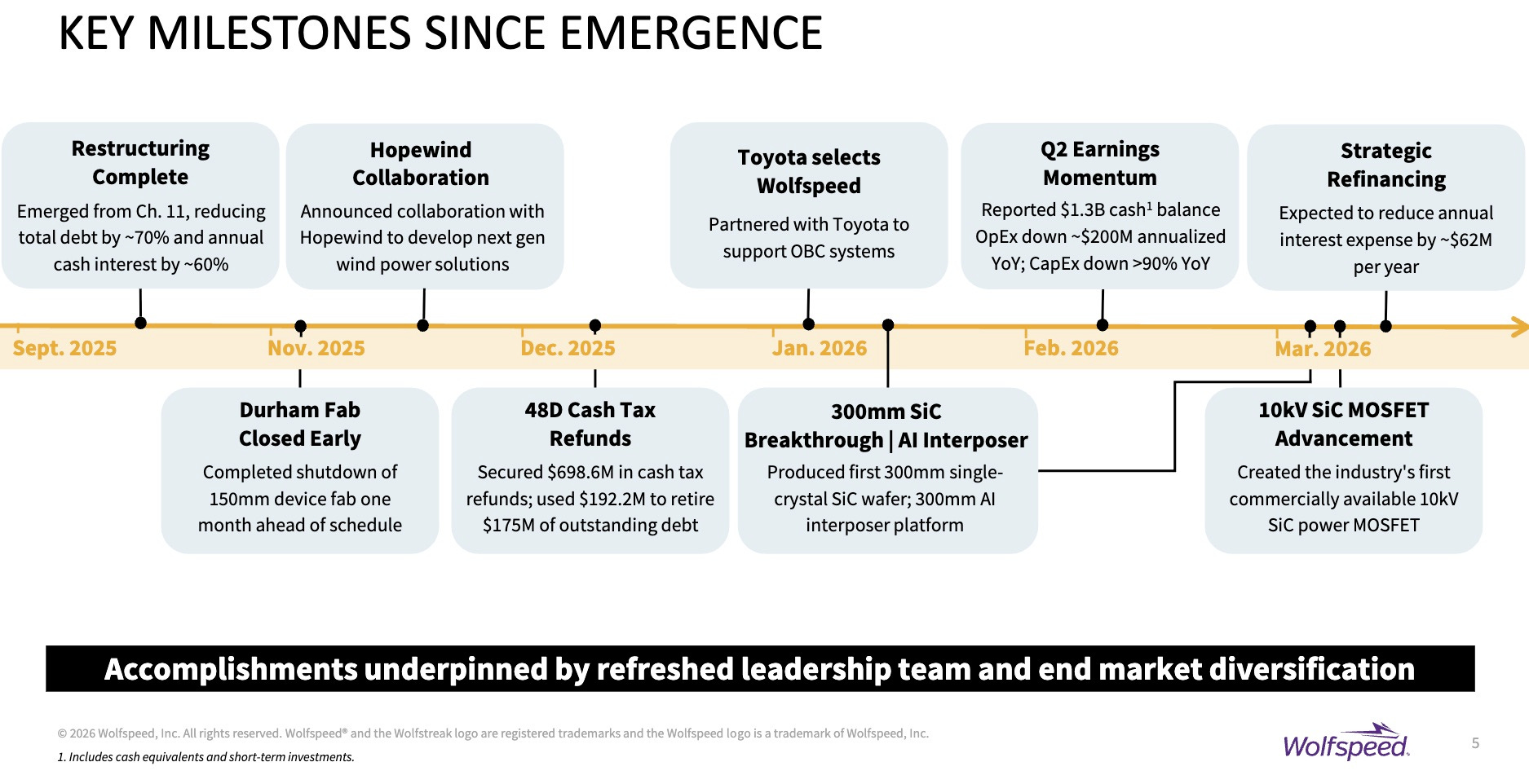

Emerged from bankruptcy with debt at $2B vs. 6B. Big progress

Key Disconnect: The market is stuck in “bankruptcy hangover” mode while the business is pivoting to AI at breakneck speed. SiC is the ONLY material that works for 800V HVDC (physics moat). Mohawk Valley at ~30-35% utilization means massive operating leverage ahead — every 10% utilization gain drops straight to the bottom line.

Also, their fabs are American.

Risk: Competition on 6-inch substrates (though not on 200mm/300mm).

Watch: May 5 Q3 FY26 earnings (AI revenue trajectory + utilization update). Design win announcements for 10kV SiC MOSFET. 300mm customer qualification milestones.

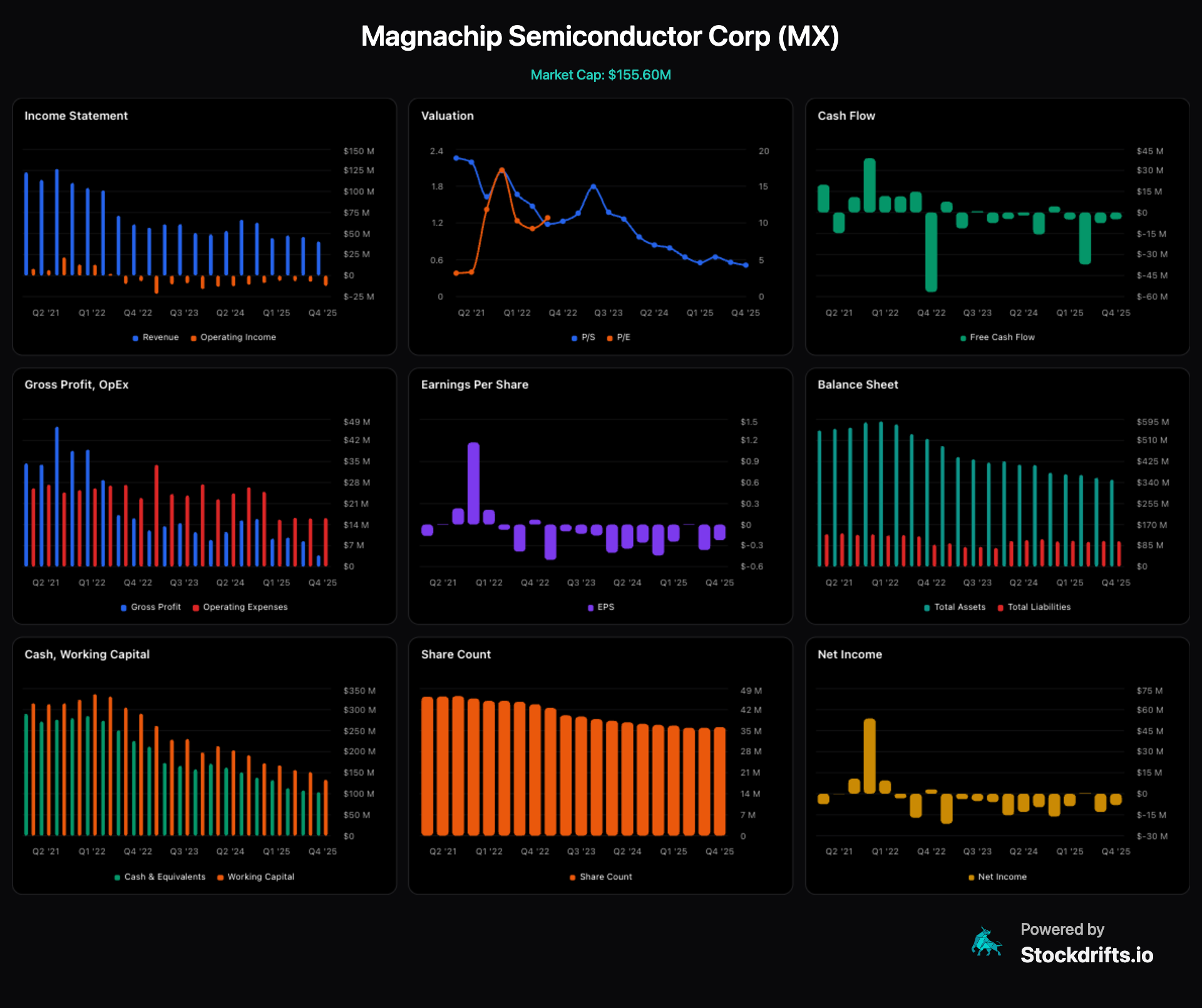

MX Magnachip: ($155M)

Cash ($103.8M) = 66% of market cap

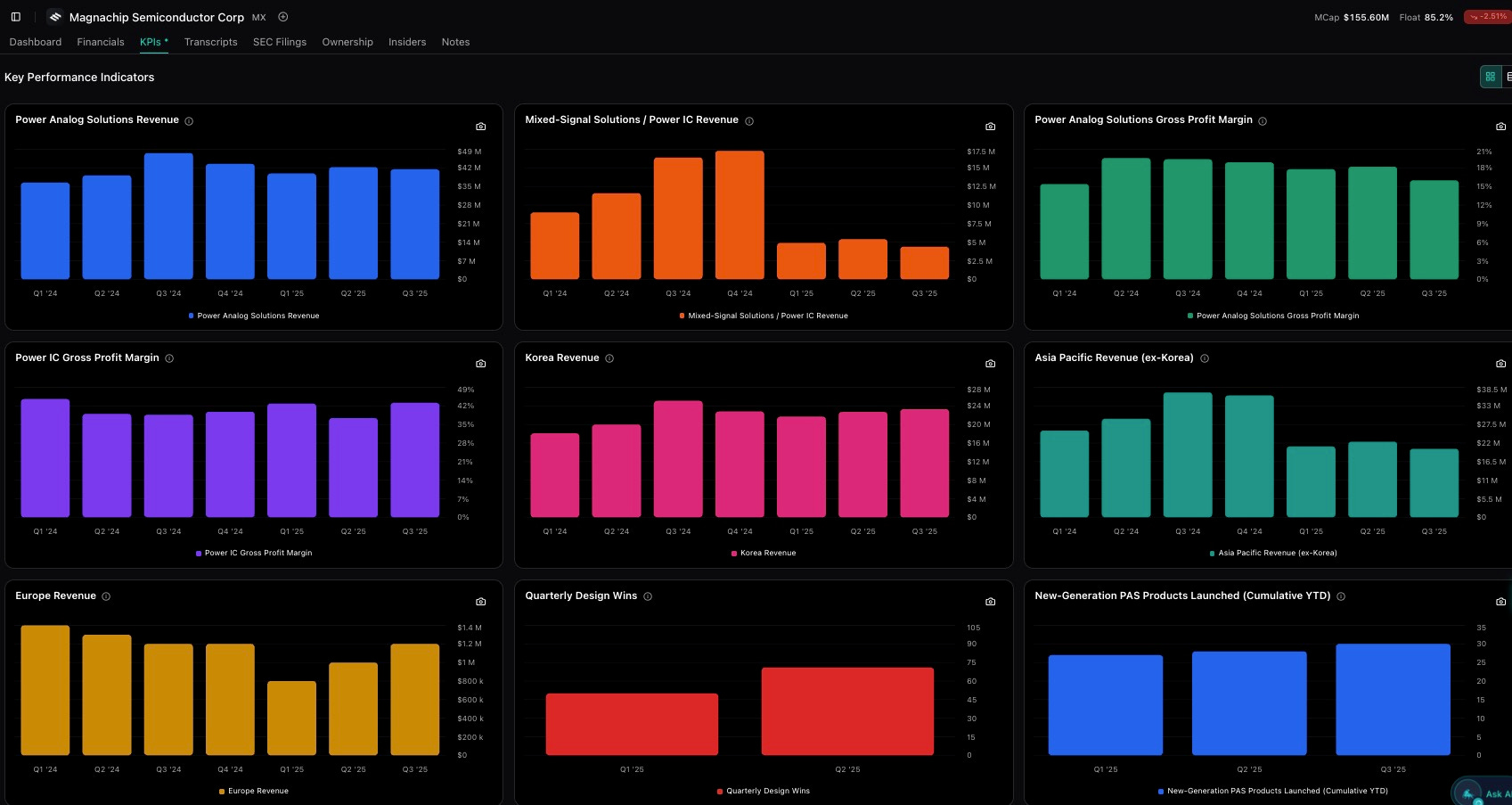

55 new products launched in 2025 vs 4 in 2024 — a 14x acceleration

They are actually buying back instead of diluting which most small caps do

Byreforge LLC filed a 13D (activist intent) for 8.5%

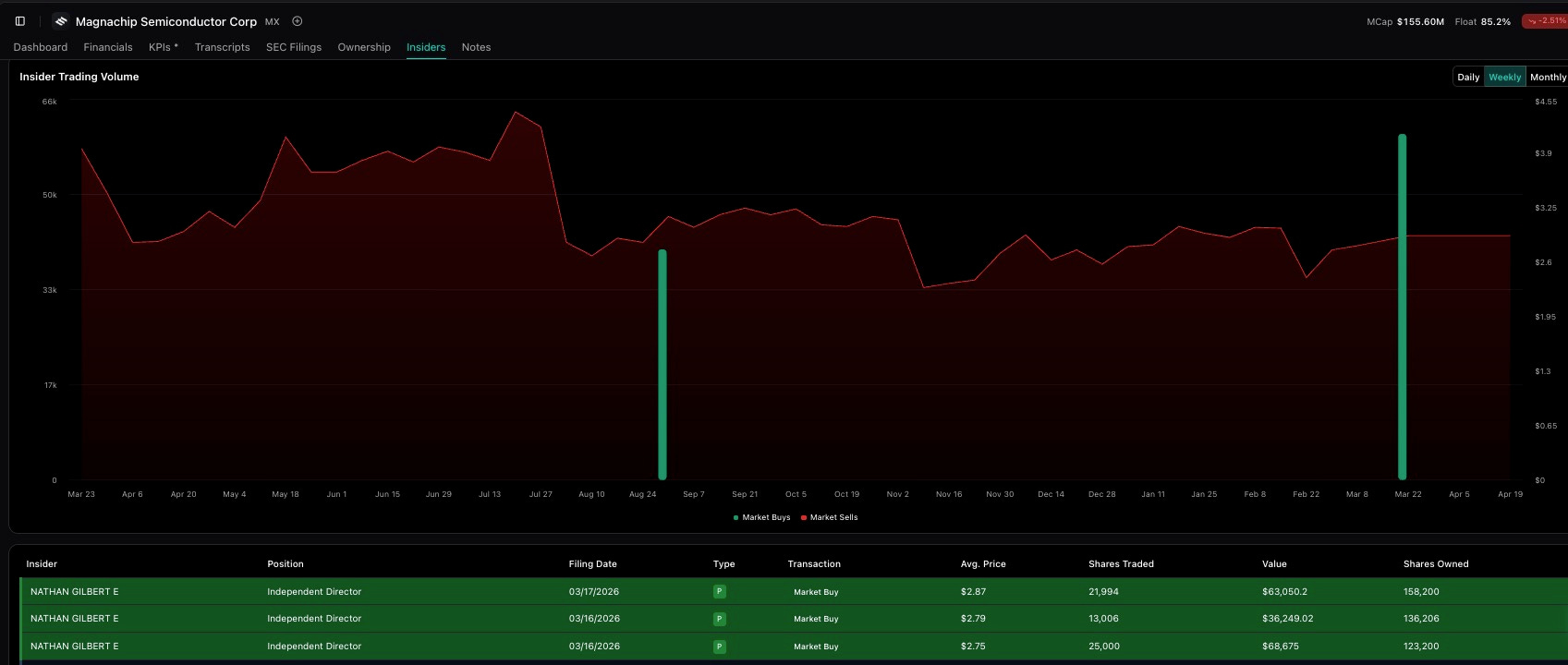

The Alpha: Market prices MX at 0.4x book as a dying display company. Reality: it’s a focused pure-play power semi company with an activist-loaded shareholder base and insider buying at every level. CEO bought 30K shares at $2.84. CFO bought 10K at $2.87. A director bought 60K shares in March

If you simply glance at the fundamentals, they don’t exactly inspire confidence. But, what’s unknown is that they decided to do a full pivot into Power semis. Sold their display business to concentrate fully.

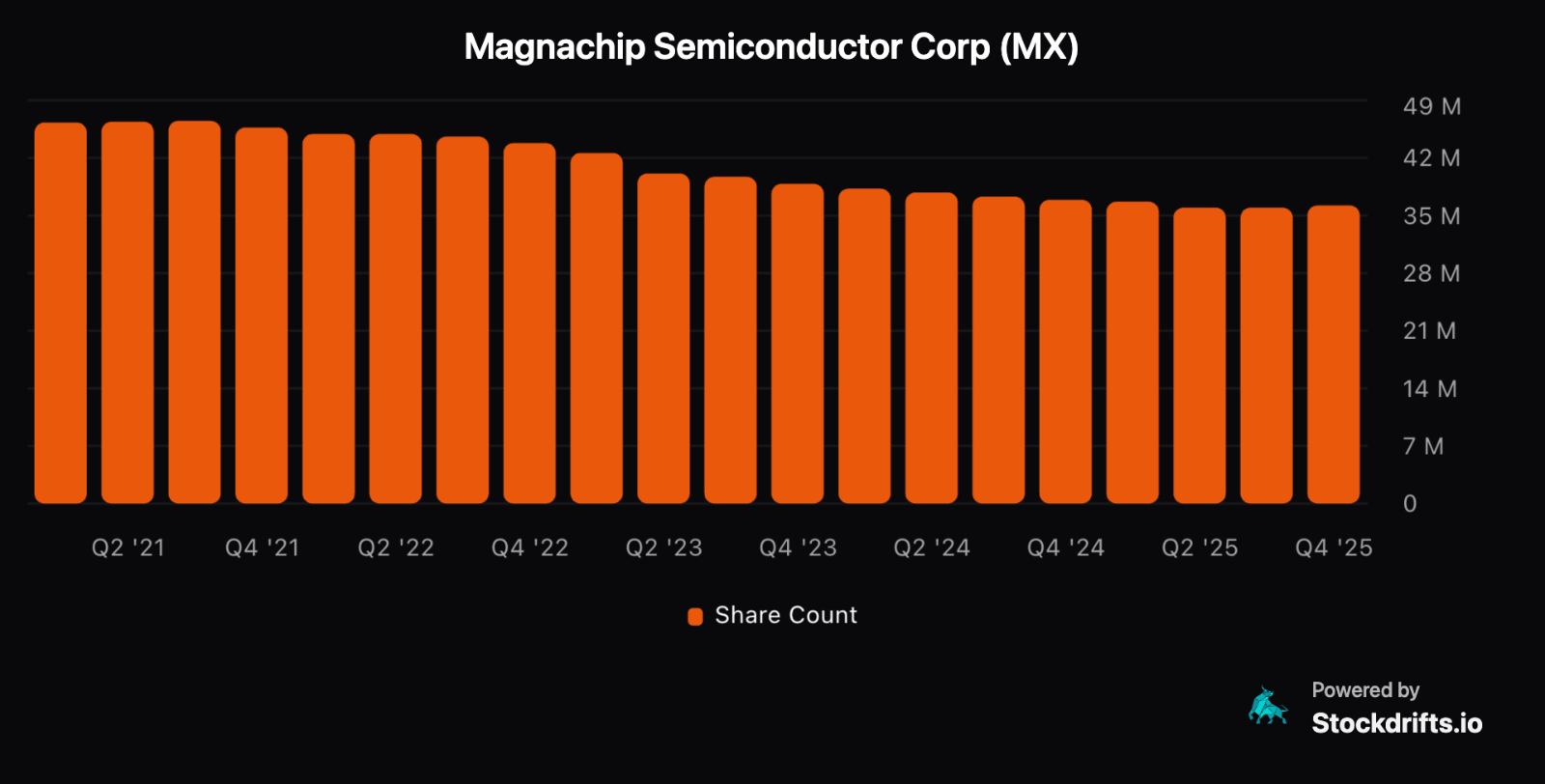

Their outstanding shares are reducing. This is a business in a turnaround stage.

Key Disconnect: The new product pipeline (40V/60V MV MOSFETs for AI servers, IGBTs for solar/ESS, Hyundai Mobis automotive JV) is invisible to the market because headline revenue is still declining from the display exit. Q1 2026 guidance shows gross margins improving from 9.3% to 14-16% sequentially — the inflection is starting NOW.

Risk: Execution risk is real. Legacy pricing pressure. Power semi revenue must ramp fast enough to offset display runoff. Competition from much larger players (Infineon, ON Semi).

Watch: Q1 earnings April 28 — this is 5 days away and the volume surge today (+22.7% on 10-15x normal volume) suggests someone knows something.

These KPI metrics do not show any improvements and hence, Analysts are clearly not pricing in the chance of growth in their business

MOSFET line (0.7mΩ Rdson, 397A, 25% faster switching, PDFN56 package) for sync rectification in the final power stage. That’s where they compete and compete reasonably well against the likes of Infineon and Alpha & Omega at that voltage class

Closing Thoughts:

I Asked Claude Code to determine the Upside Case. Do what you will with it. They are all in different Risk categories to be honest

Please no chasing. Wait for entries. WOLF and MX pumped now in the last half hour of releasing the article