We post trained a model on 4K NYSE stock's Q1-26 transcripts and used it to extract sharp insights

This allows us to have only high signal input into our model

Hello Alpha seekers,

There is so much alpha and signals and knowledge buried in Earnings transcripts. As a single analyst it is impossible to keep track of entire industries, especially when in the middle of earnings season.

Perplexity, Claude, Chatgpt all fail at this task because they got so much data that is high noise.

I will be sending more industry analysis in the coming days using this agent. For our Enterprise clients, click through auditability on transcript quotes was important, so we built it.

We are rolling this out to our Enterprise customers, so if you would like a demo, please write/DM me

DISCLAIMER: Beyond this point, the email is completely agent generated. But is incredibly insightful on finding opportunities

QUERY: What do you think are the next emerging themes/niches and are guiding for massive growth but the stock’s still yet to see that in action. Focus on AI beneficiaries

Across a deep scan of small-to-mega-cap earnings transcripts, several distinct AI-beneficiary niches stand out where management teams are describing genuine demand, raising guidance, or building entirely new product categories — yet the stock hasn’t followed. Below, I group them by theme, cite exactly what executives said, and show the performance gap.

1. AI’s “Trust Layer” — Governance, Security & Recovery for Autonomous Agents

This is perhaps the cleanest new IT spending category that barely existed 12 months ago. As enterprises deploy AI agents, the conversation has pivoted from “what can AI do” to “can I trust, govern, and recover when it goes wrong.”

AvePoint (AVPT) — CEO Tianyi Jiang, FY2026 Q1 (May 8, 2026):

“The conversation has pivoted away from productivity and towards something far more important, enterprise trust in this new enormously powerful technology… as AI agents operate more autonomously across enterprise productivity apps, companies truly need a trust layer so that they can scale AI adoption without losing control of data security, privacy and compliance.” — Tianyi Jiang, CEO · AVPT FY2026 Q1

AvePoint posted its 12th straight quarter of double-digit organic net new ARR growth and was validated by Gartner as superior to Microsoft’s native Agent 365. The company launched specific products to monitor AI agent behavior (Agent Plus), define risk for agents, and auto-remediate issues.

N-able (NABL) — CEO John Pagliuca, FY2026 Q1 (May 8, 2026):

“As we look ahead to a world with agents owning more workloads for businesses, the possibility of agents making costly mistakes also rises. We see the need to effectively undo agent mistakes and restore operations through a clean prior state as a potential demand catalyst.” — John Pagliuca, CEO · NABL FY2026 Q1

N-able is positioning its security platform as the “control plane to govern and secure agents.” ARR hit $548M (11% growth), with 106% net revenue retention.

2. AI-Powered Agent Orchestration & Analytics Platforms

Beyond the trust layer, there’s an emerging category of platforms that coordinate AI agents, build AI apps from natural language, and run real production workloads — not just dashboards.

Domo (DOMO) — CEO Joshua James, FY2026 Q4 (March 10, 2026):

“The next wave of enterprise AI will be less about models and more about coordinating data decisions and workflows… our platform doesn’t stop at insight. It unifies data, provides AI-driven intelligence via our AI service layer and with Agent Catalyst enables agentic workflows in a single system.” — Joshua James, CEO · DOMO FY2026 Q4

Domo reported record quarterly billings ($111.2M, +8% YoY), highest gross retention in 3 years (88%), and described 15 production AI agent deployments across restaurant chains, home improvement retailers, pharma companies, financial services, industrial manufacturers, and compliance tech. AI now comes up on ~70% of customer calls. The stock? Dismal.

Unity (U) — CEO Matthew Bromberg, FY2026 Q1 (May 7, 2026):

“Unity is on an incredible trajectory… strategic revenue growth of 35% year-over-year… our Vector revenue in the first quarter of 2026 is 80% larger than 1 year ago, an astonishing result.” — Matthew Bromberg, CEO · U FY2026 Q1

Unity launched Unity AI (an integrated agent that writes code directly into Unity projects) and ingests image pixels, outputs production-ready game assets. 90% of game developers already use AI in workflows, new mobile apps are up 60% YoY, and Unity expects to become GAAP profitable by Q4 2026. Yet the stock has been hammered in the near term.

Amplitude (AMPL) — CEO Spenser Skates, FY2026 Q1 (May 7, 2026) confirmed “a significant increase” in AI agent adoption on the analytics platform, deployed “forward engineers” to help customers integrate AI.

⚠️ Micro-cap risk is significant — especially DOMO at $2.42. These declines may reflect solvency or business model concerns, not just mispricing.

3. AI Infrastructure With a $553 Billion Backlog — The Stock Doesn’t Reflect It

Oracle (ORCL) is the single largest gap between AI narrative and stock I found. On the FY2026 Q3 call (March 10, 2026), CEO Clay Magouyrk:

“Multicloud database revenue grew 531% year over year. AI infrastructure revenue grew 243% year over year. Both also have demand that exceeds supply… This is directly visible in our $553 billion RPO.” — Clay Magouyrk, CEO · ORCL FY2026 Q3

Oracle has secured 10+ gigawatts of power and data capacity over three years (>90% partner-funded), signed $29 billion in new contracts since the prior quarter alone using a bring-your-own-hardware model, and hit 32% AI infrastructure gross margins (above guidance). The company is “constantly raising our FY27 forecast.” The stock: down 6% YTD, down 11% over 1 year ($184.29).

Contrast with Cisco (CSCO) — AI infrastructure orders of $5.3B YTD (4.5x FY25), Acacia optics growing 200%+ YoY, campus refresh multiyear cycle underway. Stock: +57% YTD. The market is very discriminating here — Cisco’s AI story has been bought; Oracle’s hasn’t, despite arguably larger numbers.

4. AI-Driven Drug Discovery — Faster, Cheaper, Fewer Compounds

Recursion Pharmaceuticals (RXRX) is building an end-to-end AI-powered drug discovery engine. From the FY2026 Q1 call (May 6, 2026), R&D Chief Najat Khan:

“We are synthesizing 90% fewer compounds than the industry benchmark… about 330 compounds on average versus 2,500 to 5,000 compounds… while advancing development candidates roughly twice as fast.” — Najat Khan, R&D Chief · RXRX FY2026 Q1

Recursion has 50+ petabytes of proprietary multimodal data, over 10 high-dimensional disease biology maps (half in partnership with Roche/Genentech), and clinical enrollment running 30-60% faster with its AI ClinTech tools. Phase 1 assets are now dosing (REC-4539 in small cell lung cancer). Yet the stock is down 23% YTD, down 33% over 1 year ($3.23). This is a pre-revenue biotech carrying high binary risk, but the AI moat is real.

5. AI in Legal Tech / eDiscovery

CS Disco (LAW) applies AI to legal document review. CEO Eric Friedrichsen, FY2026 Q1 (May 6, 2026):

“Overall, I’m incredibly pleased about the revenue, 14% revenue growth for the business this quarter.” — Eric Friedrichsen, CEO · LAW FY2026 Q1

CFO Aaron Barfoot added that $100K+ customer adds grew 5% sequentially and described it as a “leading indicator” — matters come in, expand, and convert to platform revenue. The Auto Review AI product is bringing in new matters and converting some to managed services. Yet the stock is down 52% YTD ($3.47).

6. AI in Compliance-Heavy Payroll & HR Systems

Asure Software (ASUR) is a small-cap payroll and HR compliance platform where AI is a moat-widener, not a disruptor. CEO Patrick Goepel, FY2026 Q1 (April 30, 2026):

“We move approximately $20 billion annually on behalf of our clients… These are not functions that a generic AI layer can absorb. The regulatory complexity does not go away. In fact, it compounds.” — Patrick Goepel, CEO · ASUR FY2026 Q1

Revenue grew 23% YoY to $42.8M. Organic growth accelerated to 7% (from 3% in Q1 2025). Luna, the AI agent, saw interactions up ~50% QoQ, adopted by >15% of potential users with zero marketing. The AI layer is converting manual compliance workflows into proactive continuous systems, and the new AsureWorks managed service brings 2-3x the revenue of a payroll-only client. Stock: down 9% YTD ($8.27).

7. Edge AI Fiber & Distributed Compute Infrastructure (Early Stage)

Clearfield (CLFD) is a small-cap fiber company pivoting toward edge AI infrastructure. CEO Cheryl Beranek, FY2026 Q2 (May 6, 2026):

“Industry trends continue to support a shift toward compute closer to the end user, as low-latency AI applications require faster processing capabilities… This dynamic will drive the build-out of smaller distributed edge locations that function like compact data centers and require high-density fiber connectivity.” — Cheryl Beranek, CEO · CLFD FY2026 Q2

Backlog rose 39% sequentially (1.3 book-to-bill), the NOVA Platform for edge AI ships in H2, and BABA-compliant fiber extrusion is ready. The stock is up 37% YTD but only +5% over the past year — early recognition of the thesis.

Dycom (DY) — EVP Dan Peyovich on the FY2026 Q4 call (March 4, 2026) described a $20B+ TAM for AI-driven long-haul and middle-mile fiber construction:

“Is it more than $20 billion? We strongly believe that… today, we are getting more phone calls and seeing more opportunities than we saw even a quarter ago or, frankly, even a week ago.” — Dan Peyovich, EVP · DY FY2026 Q4

Dycom’s fiber-for-AI story is back-half weighted, ramping through 2027-2028. Stock is up 31% YTD (+97% 1-year) — partially discovered.

8. Inference Economics & The Token Multiplier

Multiple CEOs flagged the same inflection: agentic AI drives 5x-30x more tokens per task vs. simple chat. This means the inference economy is radically underbuilt.

Digital Realty (DLR) CTO Chris Sharp, FY2026 Q1 (April 23, 2026):

“As agents come to market, it’s a demand multiplier… 5x to 30x more tokens per task… that’s going to really drive another inflection point.” — Chris Sharp, CTO · DLR FY2026 Q1

MARA Holdings (MARA) CEO Frederick Thiel, FY2026 Q1 (May 11, 2026):

“We’re seeing thousand-fold increases in agentic token consumption when somebody moves from chat to using Cowork or Claude Code… Just talk to any CIO and ask what their token bills are lately.” — Frederick Thiel, CEO · MARA FY2026 Q1

DLR is up 21% YTD; MARA is up 43% YTD. The inference hosting/token factory thesis has partial recognition but is still early.

✅ Already Priced In: Themes Where Stocks Have Moved

For clear contrast, these AI beneficiaries have seen massive price action — the narrative is well-understood by the market:

Key Takeaways

AI Trust & Governance is the freshest unmet theme. No company I found has a clearer story than AVPT and NABL — both explicitly building the security and control infrastructure for autonomous agents, both growing ARR double-digits, both down 20-60% YTD. The risk is that platform giants build native governance, but these companies are pre-integrated and validated.

Oracle has the biggest narrative-to-price gap of any mega-cap. A $553B RPO, 531% database cloud growth, and $29B signed in three months at improving margins — yet the stock is down YoY. This is a puzzle the earnings calls repeatedly flag: “the market has yet to recognize” is a recurring management theme.

The AI agent orchestration plays (DOMO, AMPL, U) are heavily beaten down but pivoting hard. Unity’s 35% strategic revenue growth and Vector AI scaling, Domo’s 15 production agent deployments, and Amplitude’s agent adoption surge are real. These names carry execution risk and micro/small-cap survivability concerns.

AI Drug Discovery (RXRX) and AI Legal (LAW) are longer-duration bets. Both have real AI differentiation (50PB data, 90% fewer compounds; 14% revenue growth, expanding $100K+ customers) but the stocks need catalysts — clinical data readouts for RXRX, sustained revenue reacceleration for LAW.

The inference token multiplier is a theme everyone is talking about but few are positioned for. DLR’s CTO on 5-30x tokens, MARA’s CEO on thousand-fold increases — the buildout of inference infrastructure (token factories, private AI clouds, edge compute) is a multi-year wave where the capital hasn’t fully deployed yet.

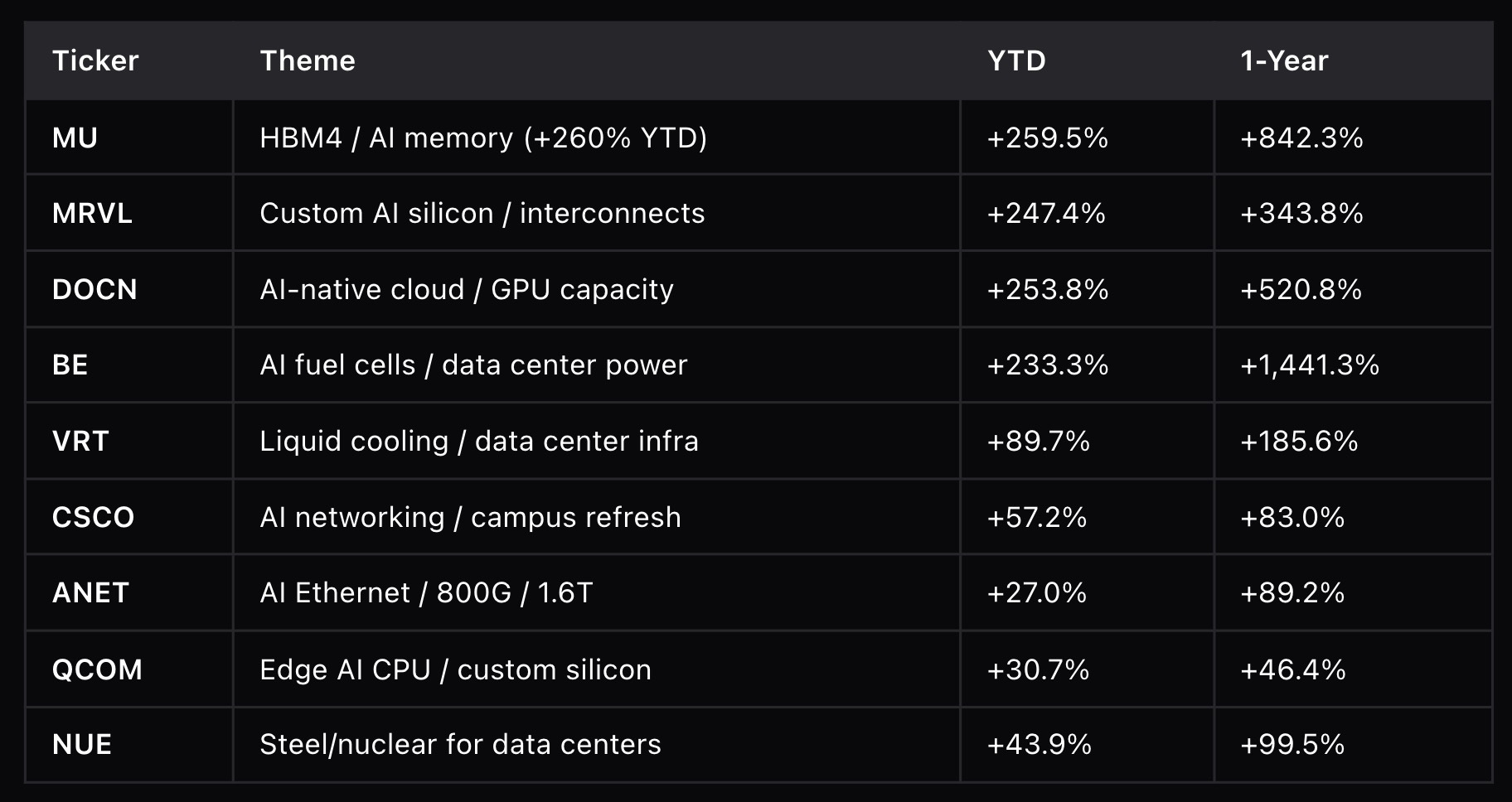

The market is discriminating sharply. Memory (MU +260%), custom silicon (MRVL +247%), and copper/fiber/cooling (BE, DOCN, VRT) are well-recognized. The next wave of recognition seems most likely in AI governance/trust and in the companies building the software orchestration layer for agentic AI — but those are smaller, riskier names.

Wow. What an update. Really smart!!

Did you check Agents++ from Abaxx Technologies, which addresses the AI security issue?