Utility grade Solar Supply Chain

$TE, $TOYO $TSLA $GLW etc.

TLDR: Pure US supply chain is elusive in the short term

All hell broke loose when Tesla said they are entering the Utility Solar game by vertically integrating and targeting 100GW production

Spoiler Alert: $TE will do just fine!!

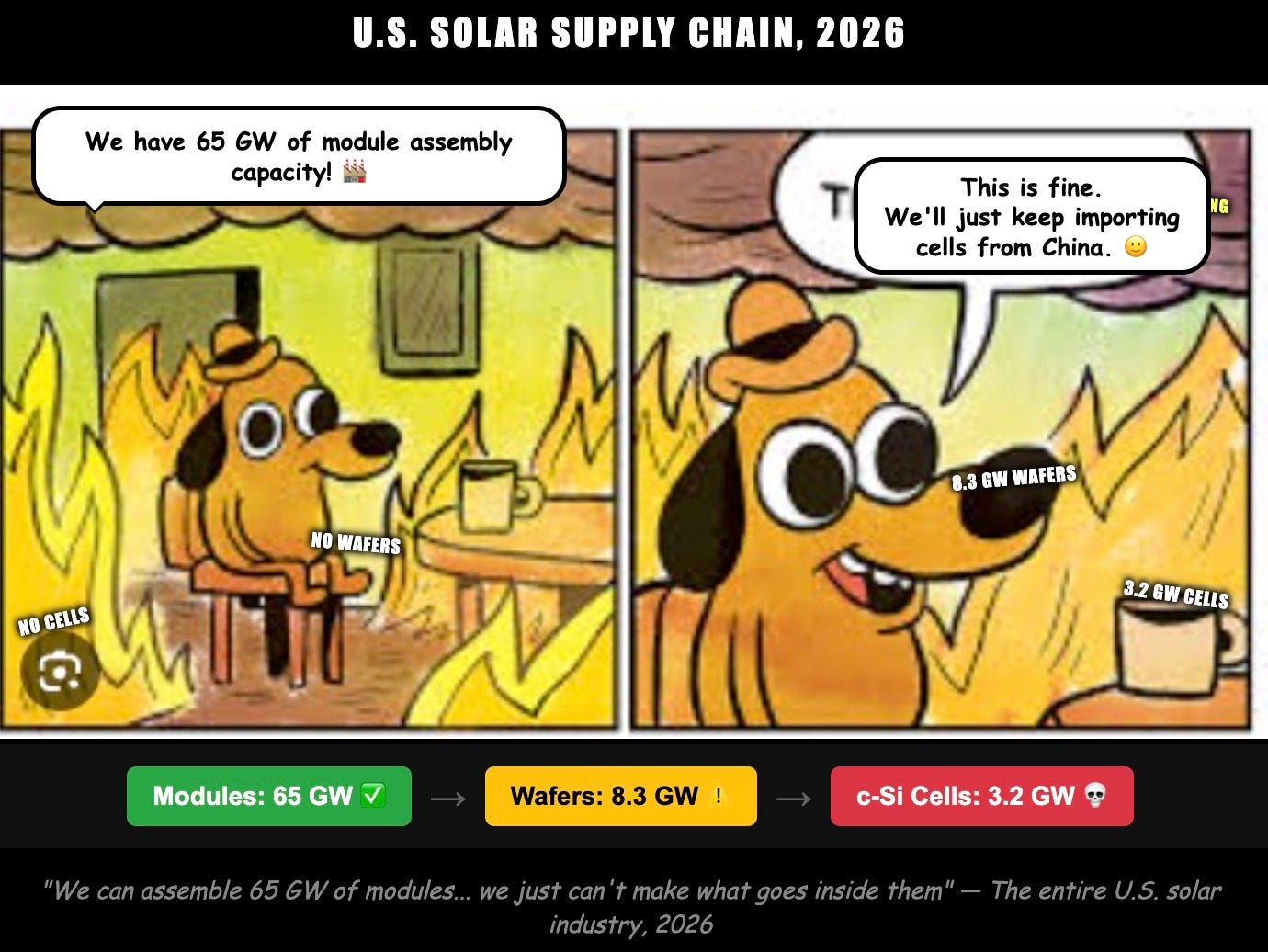

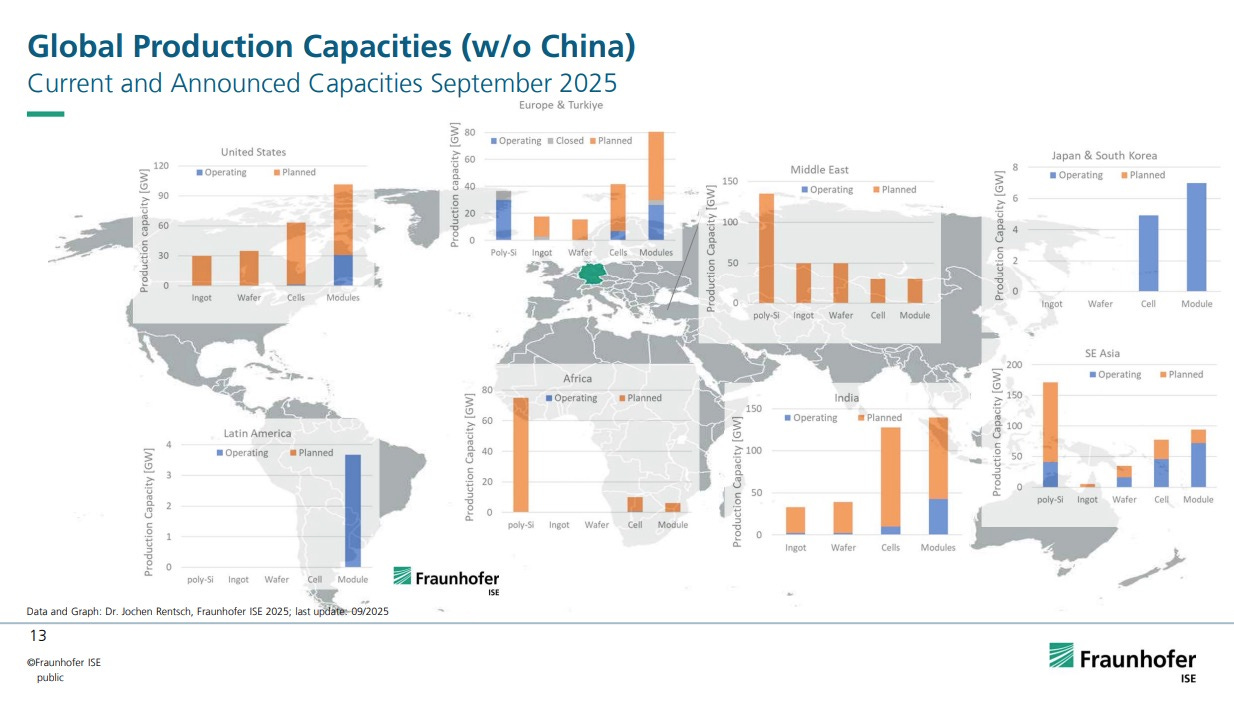

Module assembly capacity has surged to ~65 GW annually, HOWEVER, the supply chain remains imbalanced with only ~8.3 GW of wafer capacity and ~3.2 GW of c-Si cell capacity domestically

Okay while we scratch our heads over that, there is an S&J’s interview with TE’s VP this Thursday. Definitely don’t miss

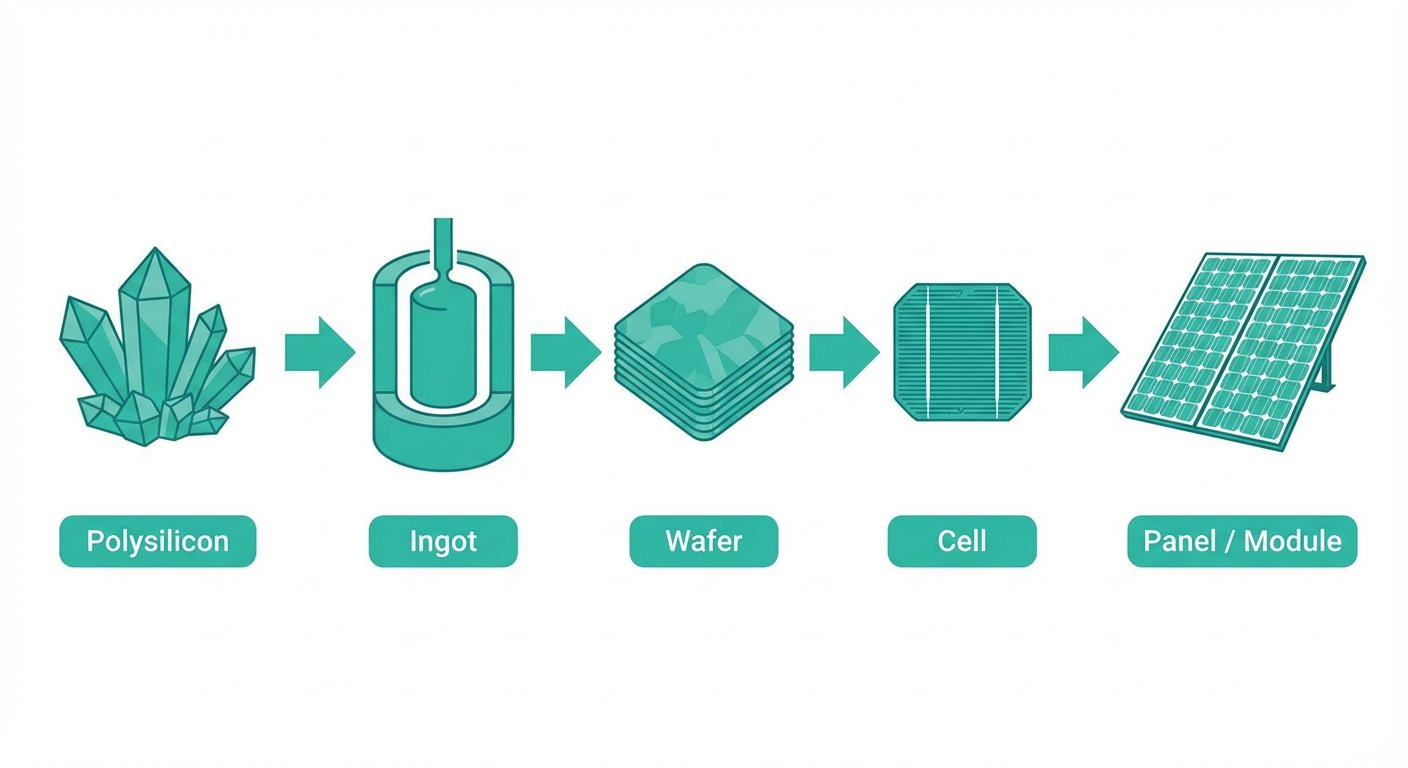

Okay, lets look at the supply chain that exists. 5 steps to get to that sweet sweet Solar Panel

Supply chain capacities across the world

This chart allows you to appreciate the mismatch and how the dream of full vertical integration is still far far away.

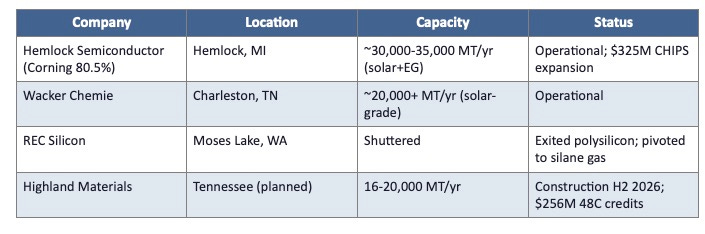

STAGE 1: POLYSILICON

Combined US nameplate: ~50-55K MT/yr. Actual production ~33K MT. If all of that was converted into Solar cells it would be equivalent to ~13-16 GW of solar modules.

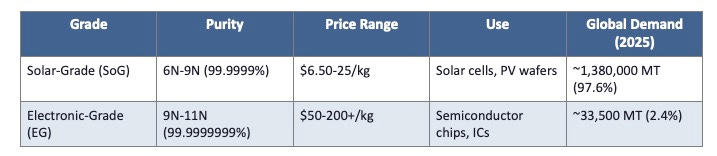

Keep in mind that Polysilicon is also required for semi conductors. Albeit the grade gotta be much purer than solar. 98% of Polysilicon is used for Solar

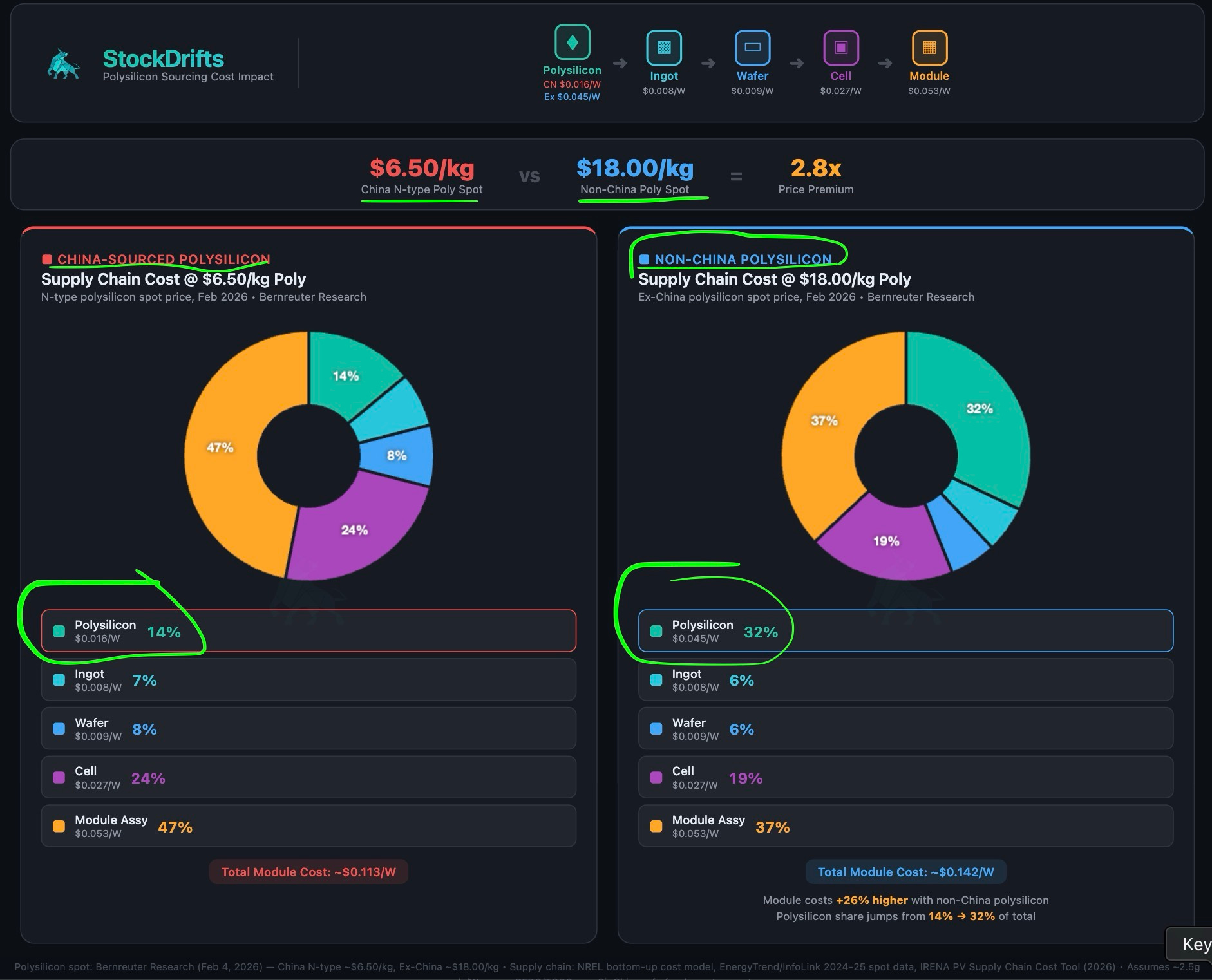

The real issue is that the 45X Credit: $3/kg only and the gap between Western polysilicon and Chinese is around 12$. So that really is a big gap. Pure, US supply chain is going to come at a short term cost. Not to mention there is simply no capacity for Polysilicon in the US

I think that TE, TOYO and eventually Tesla might do the most minimum possible to satisfy FEOC. They are eating glass or paying 3 times the price to get US Polysilicon.

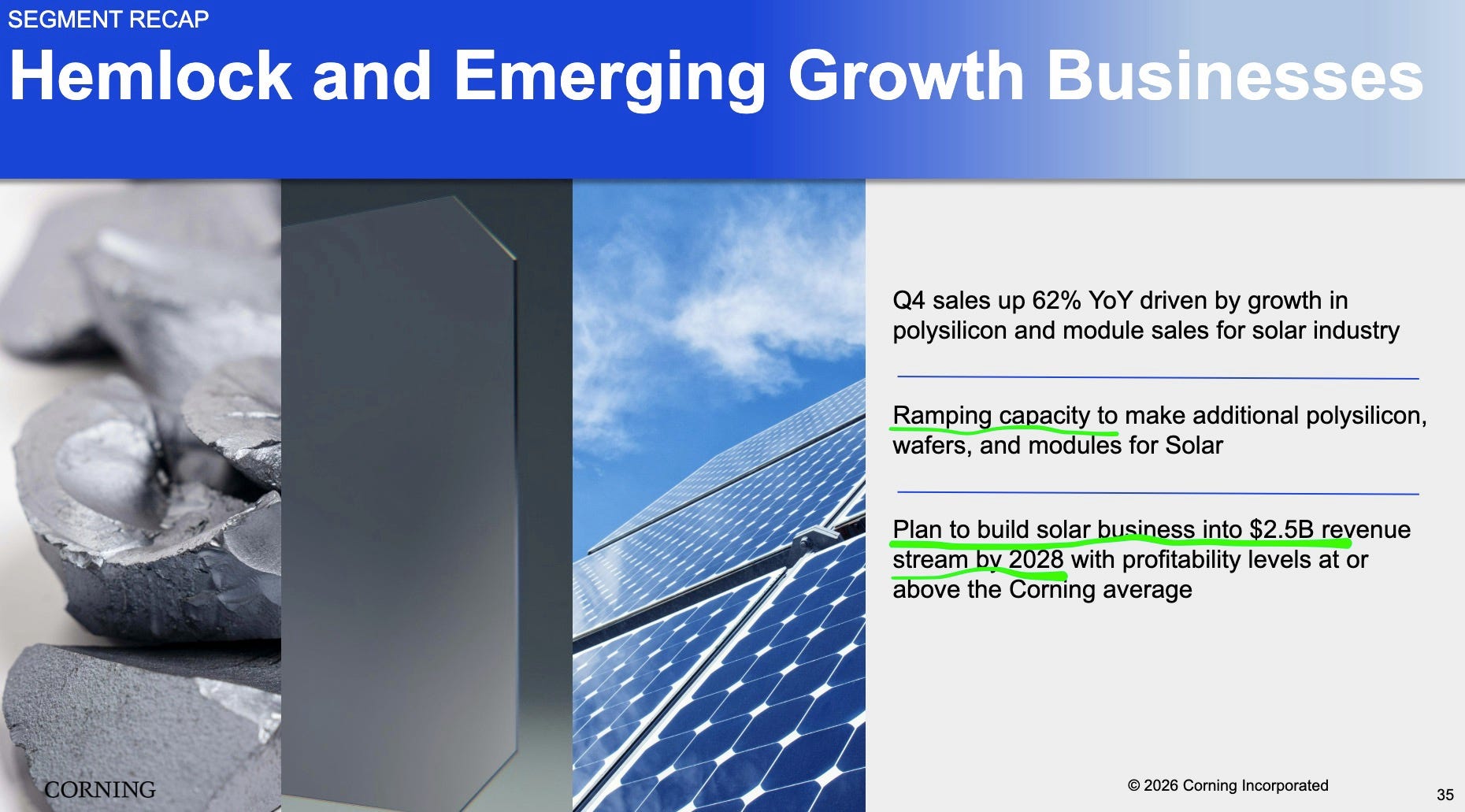

Atleast the Good news is that we can see Corning GLW 0.00%↑ promising to increase the production massively. These infrastructure companies do not simply increase capacity. They do it when there is massive shortage.

It is also an indication that the demand is through the roof for Polysilicon if GLW is planning to exponentially increase their Solar revenue.

Lastly, I spun up Claude code Python to calculate the difference. When you source from Non China Polysilicon, it suddenly becomes 1/3 your total costs.

I think there is a lot you can do to mitigate this. For eg. Credits might help and some more financial sorcery.

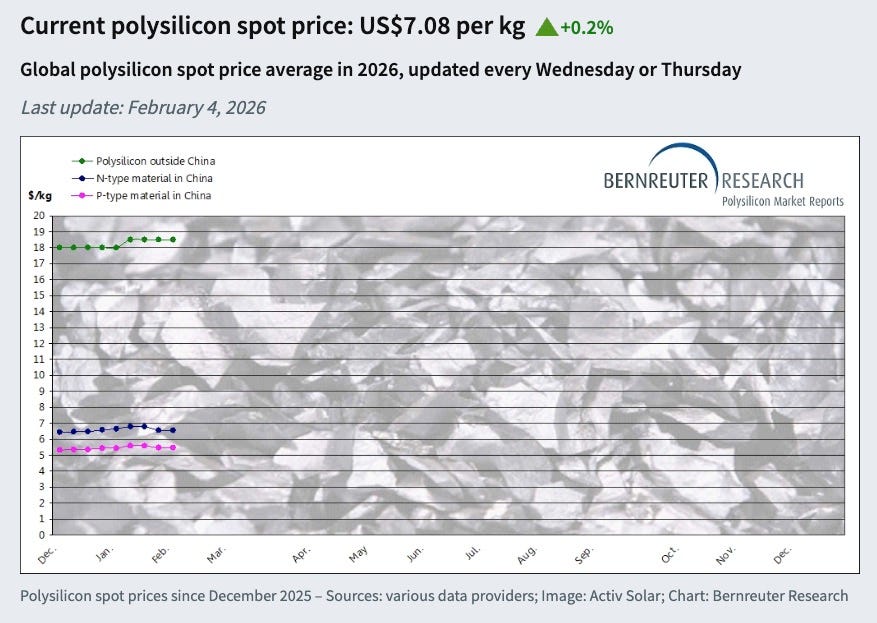

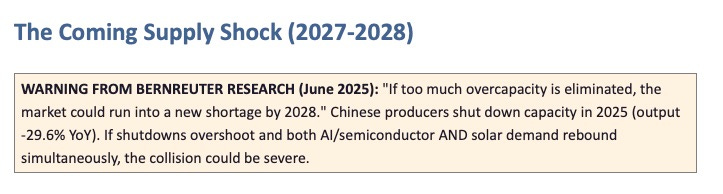

Lets see if this really comes through in 2027-2028. However, it did happen that a lot of Chinese supply shut down and Polysilicon prices bounced up ~30-50% up.

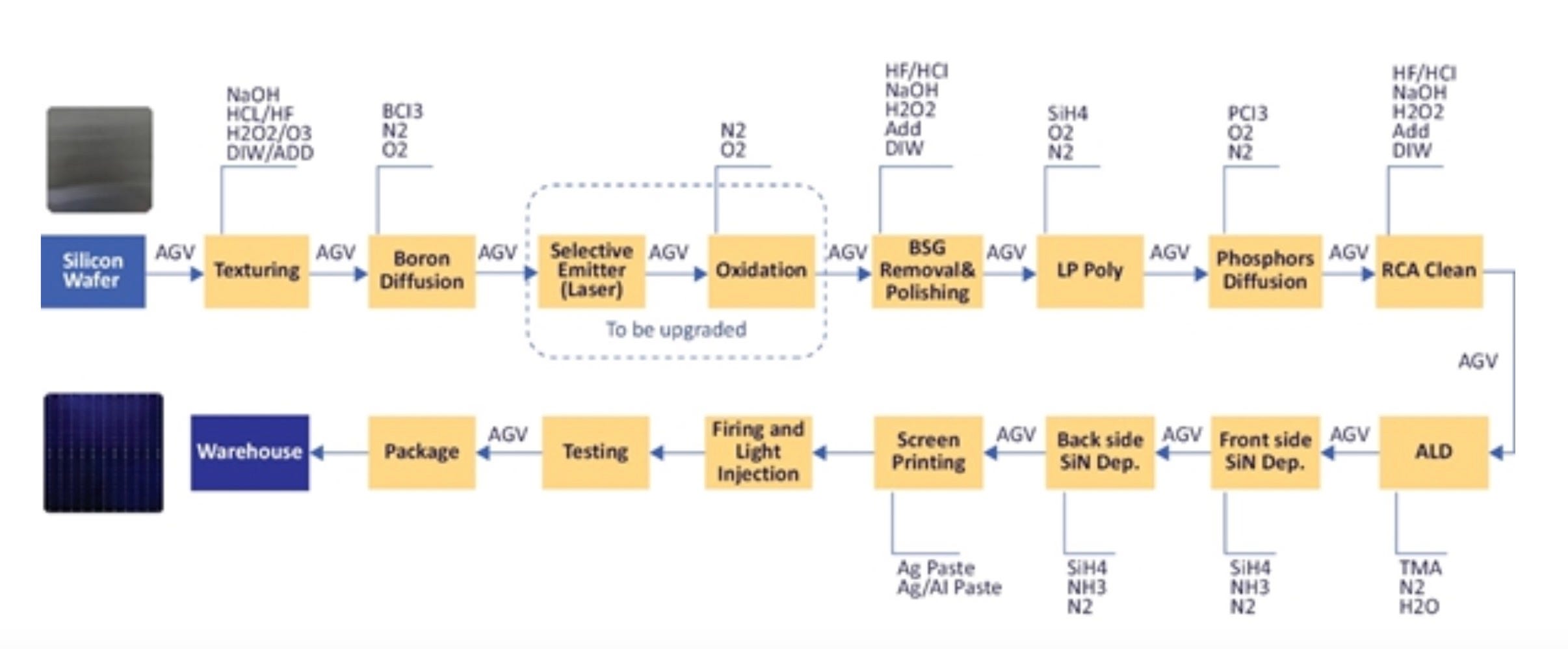

Also P.S. cell-level cost is deceptively low; a company’s success ultimately depends on the quality of its cell manufacturing process. Because a better manufacturing process means higher efficiency for the panels. And even a little bit more efficiency over its lifetime of a few decades can compound quickly.

Have a look at how Solar cells are produced.

I am sure Elon will delete a LOT of steps and rethink the whole industry from fundamental point of view, however the reality of things are still going to be that having American Solar supply chain is not a short term target.

I am planning to give away all of my Solar watchlist to Annual subscribers. My favorite small caps or best multibagger opportunities with liquidity in the space.

I have been sitting on it for far too long. Will also release interesting watchlist in other themes as well.

Do you still like BWEN?

I really think GLW is still very cheap and might pull a SNDK type run