Robotics Bottleneck play (~$4B)

Also the ONLY Western supply chain player in it's niche

I was writing an in depth article on a Robotics bottleneck play.

Serenity unfortunately just now mentioned it and I am forced to release my half baked article.

If you have money in your IBKR account, you could get in on Sunday late night (Japan’s stock market open) and play along.

I started mentioning this name to my inner circle in March. I will start publishing my early ideas more often. I want you to consume them before the swarms of bees arrive. Maybe in a chat community.

I have a bigger article coming up on how inflation is here to stay and is going to be structural. OPEC talked about loosing 30% of their production capacity. And Cathie is delusional (Again) when she says tech is going to cause disinflation.

Lets begin

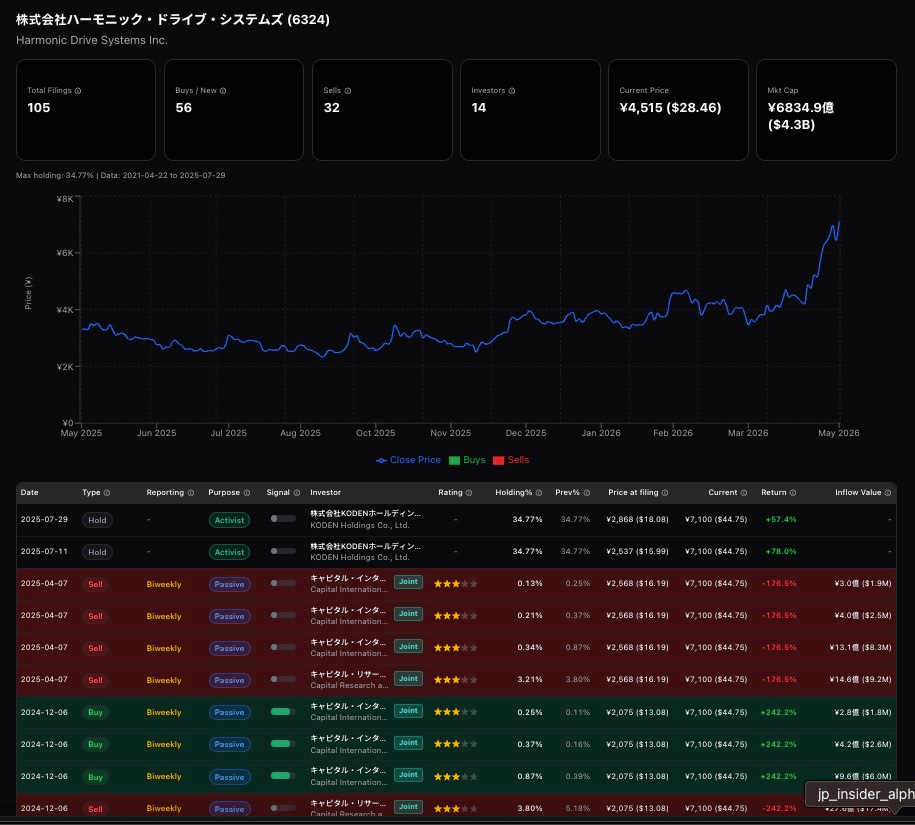

HARMONIC DRIVE (6324)

Here is the short thesis

- Every humanoid uses 10–40 strain-wave actuators per unit at $2k–$5k each → arguably the single highest-margin BOM line in the robot. There is literally no other western provider for this except Harmonic drive

A strain wave gear (aka harmonic drive) is the precision reducer that turns a fast, weak motor into the slow, high-torque, zero-backlash motion a robot joint needs.

Three parts: an elliptical wave generator spins inside a flexible steel cup (flexspline) whose teeth mesh, at two points, with a slightly-larger-toothed outer circular spline. Each motor revolution advances the output by only a few teeth → 50–160× reduction in one stage, sub arcminute backlash, very high torque density.

- Micron-level grinding and flexspline metallurgy are the moat.

Only real challenger: Leaderdrive / Green Harmonic (688017.SH), which already supplies Tesla Optimus and owns >60% of China domestic share. Nidec, Sumitomo (cycloidal alt.), and a handful of Korean startups (e.g. SBB Tech) chase.

- Closest analog: ASML in lithography — one Japanese firm holds the precision-machining know-how the rest of the industry needs to scale.

1. Why HDS holds the chokepoint

The thing isn’t really “harmonic drive” the product — it’s strain wave gearing, a category invented by C. Walton

Musser in 1955. That original patent is long expired; HDS’s moat today rests on three layered things:

- Tooth-profile IP. HDS owns the modern profiles that actually work — the “S-tooth” and “IH-tooth” geometries that get ~30% of teeth in continuous engagement (vs. far fewer in involute gears). That is what gives the unit zero backlash, sub-arcsecond repeatability, and high torsional stiffness in a pancake form factor. Patents extend to lubrication sealing, dual-stress separation (US 10,788,114 — Ishikawa 2020), and powder lubricant delivery.

- Process know-how. Flexsplines are thin-wall hardened steel that has to fatigue-cycle hundreds of millions of revolutions. Heat treat, grinding, and surface finish tolerances are deeply tacit — patents don’t tell you how to actually make them survive. This is the harder-to-copy layer.

- Reference designation. In semiconductor lithography, surgical robots, satellites, and high-end SCARA/six-axis arms, HDS is the de-facto spec. Once you’re in a customer’s CAD and qualification dossier, you’re in for a decade.

2. Can they be innovated out?

Partially yes, already happening — but only at the low/mid end:

- Chinese challengers (Suzhou Green Harmonic, Leader Drive) sell harmonic reducers at 40–60% of HDS price and have ~25% global share. Green Harmonic is bringing a 500k-unit/yr Suzhou plant online in 2026 specifically for humanoid demand.

- For commodity humanoid joints, “good enough” precision + cost will erode HDS’s unit share. Tesla’s strategy of dual-sourcing HDS + Green Harmonic is exactly this — qualify the Japanese gear for early bring-up, ramp on Chinese gear when volumes arrive.

- For sub-arcsec / aerospace / semicap / surgical, the manufacturing moat still holds. No credible substitute has emerged — RV/cycloidal (Nabtesco) is heavier and used at the base joints, planetary roller screws are linear-only,and magnetic gears haven’t matured.

So: HDS can be innovated around at low precision but probably not replaced at the high end inside a 5-year horizon.

The real risk is mix shift — they own a smaller piece of a much larger pie.

3. Does Tesla buy from them?

Yes, but not exclusively, and there is no publicly disclosed direct purchase agreement. Industry supply-chain teardowns (China Merchants, 36Kr, futunn) consistently list HDS alongside Suzhou Green Harmonic as Optimus harmonic-reducer suppliers. Tesla Optimus uses 14 rotary actuators, each = frameless torque motor + harmonic drive + sensors. Tesla’s known posture is dual-source; the $685M Sanhua order was for thermal/linear actuators, not harmonic gears.

HDS itself has not disclosed Tesla as a named customer in any IR document I can find — they discuss “robot manufacturers in Japan/China/Europe” generically. So treat the Tesla angle as strongly inferred from supply-chain reporting, not company-confirmed.

RISKS:

No insider buys in the last year. I am scratching my head on this one. Stockdrifts has Japanese and Korean stock insider graph.

Schaeffler just changed that.

€16B in revenue. Automotive-grade manufacturing infrastructure. An RT actuator platform designed from day one for high-volume production. Already 45 humanoid partnerships globally, 5 major contracts signed, and a self-reinforcing model where they deploy robots in their own factories to stress-test their own components. The moat around Harmonic Drive was always scale and Western supply chain trust. Schaeffler is the one Western bet I'm actually willing to make in the humanoid actuator race.

Excellent thesis. The supplier qualification dynamic is what makes this position especially interesting: humanoid OEMs need at minimum two qualified sources for supply chain security, but Green Harmonic (688017.SH) hasn't yet demonstrated consistent quality at their claimed 500k unit/yr capacity.

Until they do, Harmonic Drive retains the socket.

The moat-break signal to watch: whether Tesla, Figure, or Agility publicly qualify Green Harmonic in a regulatory filing or earnings call. That's the specific catalyst that matters here — not Green Harmonic's capacity announcements.

Tracking this closely at Humanoid Alpha — great post, would love to exchange notes on the qualification timeline.