Initiated a SPEC position in a new Battery Energy name

I am excited to dive deep

I had been eyeing this Battery stock for a very long time and it’s been looking at me seductively. But finally now I pulled the trigger and initiated a speculative initial tranche.

They raised convertible debt and crashed the stock. And we know what means. Ask EOSE investors at $4, TE investors at $3.25, or ASTS investors at $3

If you have been looking to invest in alternative grid scale Batteries and never got around to EOSE, here is a really interesting stock <$1B market cap

Before I talk about this stock, lets set the stage right. After the disastrous earnings of FLNC with suppressed margins and having to move around Battery supply chains through 3 different US facilities in order to chase them 45X credits, it’s time to look at something new

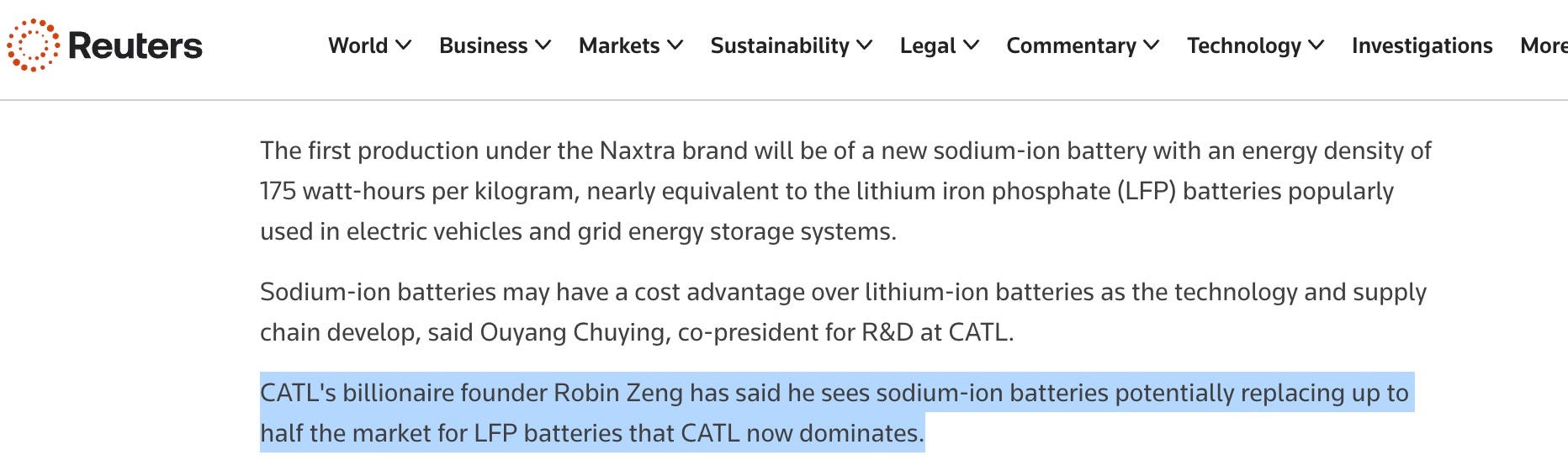

Here is CATL’s Founder Robin Zeng saying that Sodium Batteries can displace 50% of the LFP battery market last year

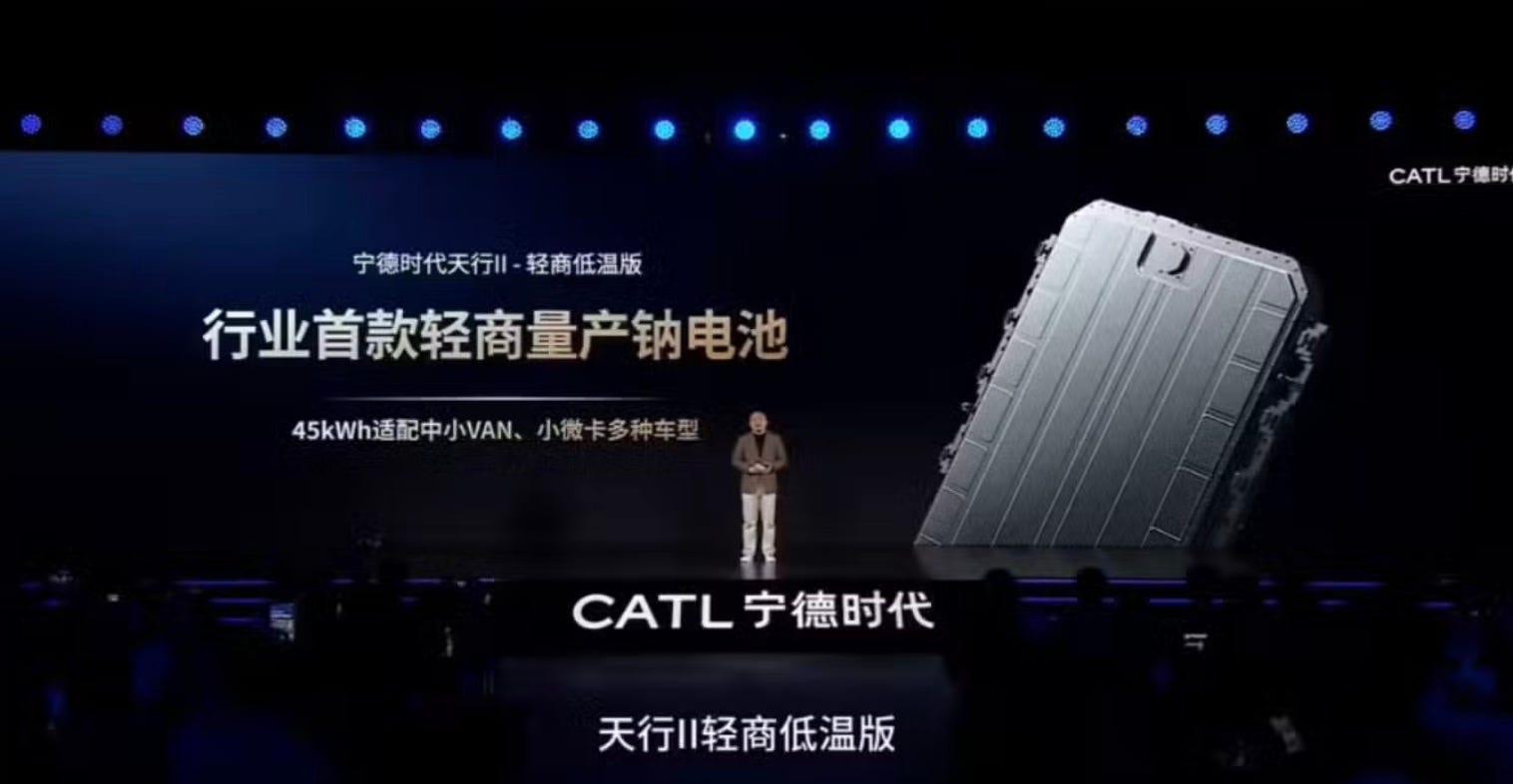

They officially launched it in production 2 weeks ago

There is a way to get exposure to the Western/American Sodium Batteries Via NRGV 0.00%↑

I wanted to get this report quickly. But in the subsequent deep dives, I will attach a video from my discussions with Battery expert Jordan G from The Limiting Factor Youtube Channel

“Sodium Ion Batteries are better than Lithium Ion LFP batteries in every way. Cheaper, easier to scale, more abundantly available, less risk of fire”

But then we also discussed how LFP batteries enjoy economies of scale and by the time other alternative forms scales LFP batteries would have moved the goal post

I talked about how Javascript is a an inefficient framework, but it STILL took over the world because it was a first mover and early and had network effects.

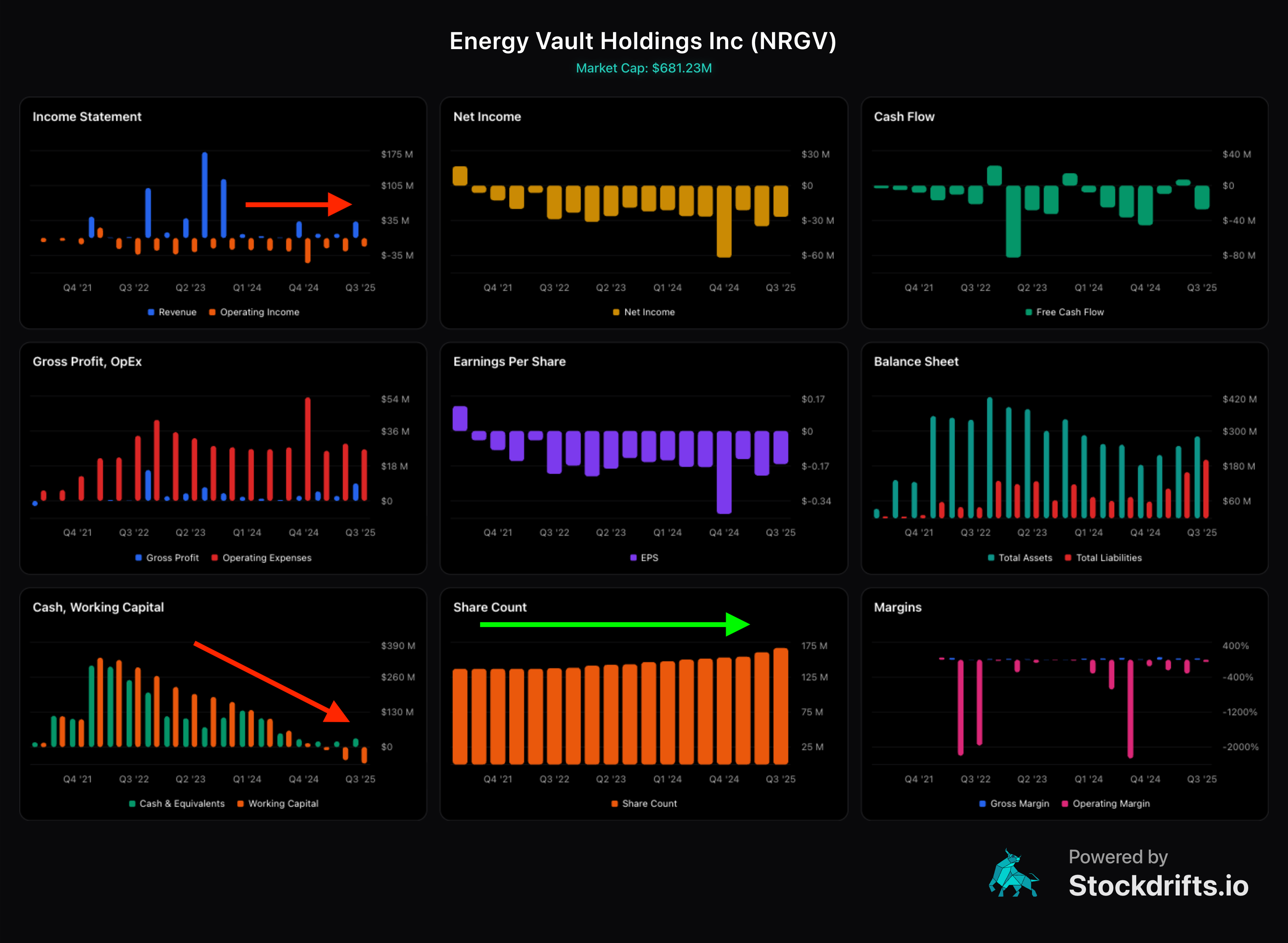

With that said, lets jump into NRGV 0.00%↑ snapshot.

Technically they are at a perfect point to get in, if the fundamentals are right

Consolidation and a Retest with volume

Here is what I like about them:

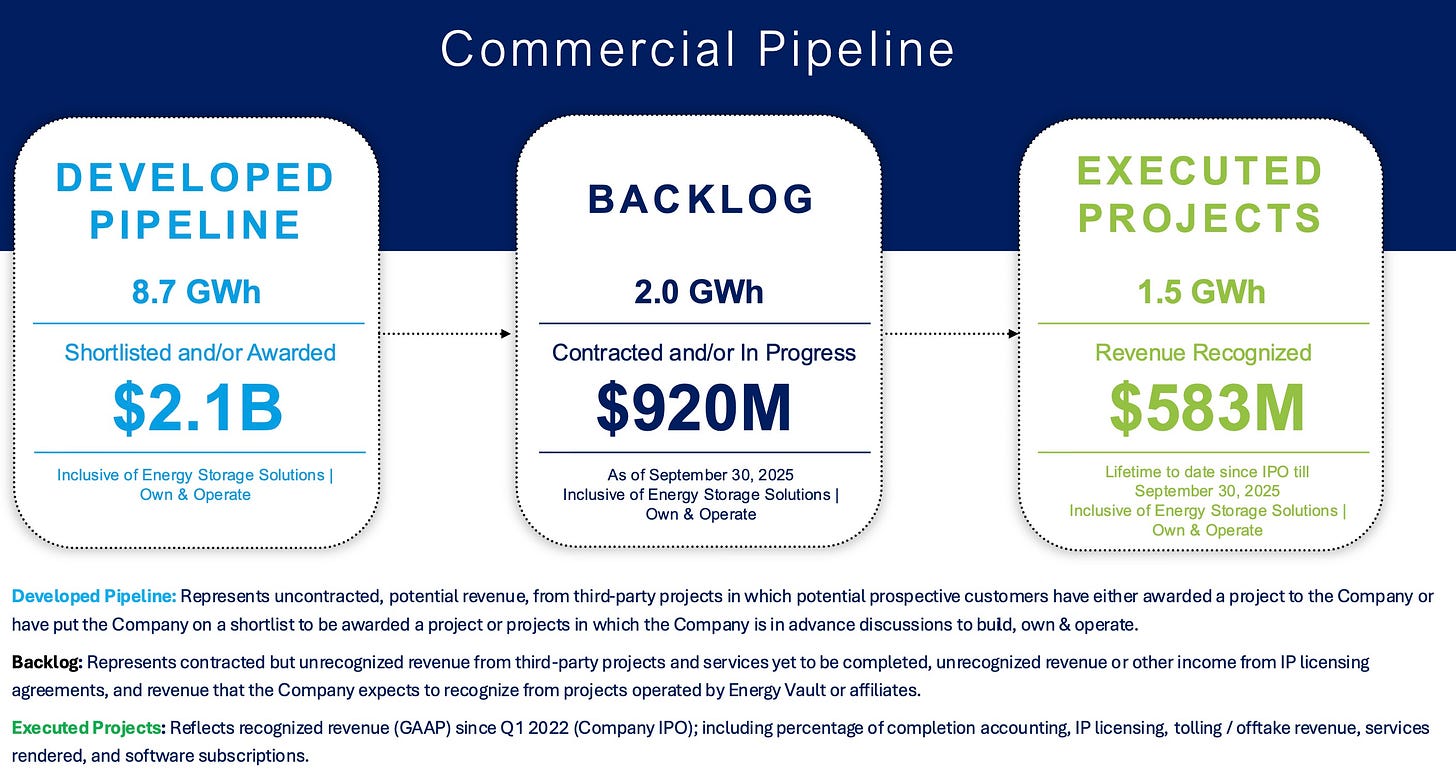

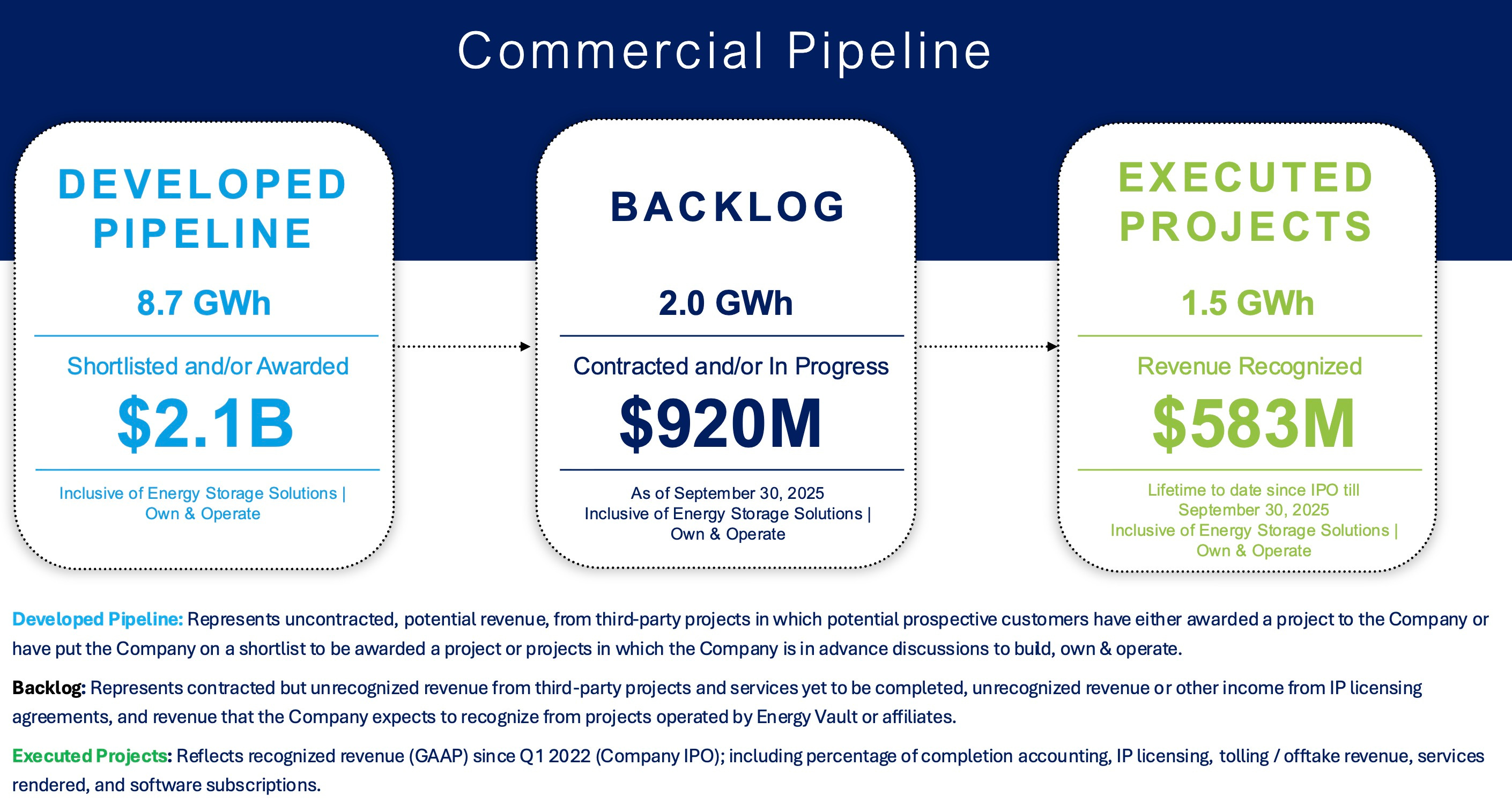

Revenue backlog of ~1GW

Ownership model rather than . Assets predicted to generated $40M EBITDA per year now and growing

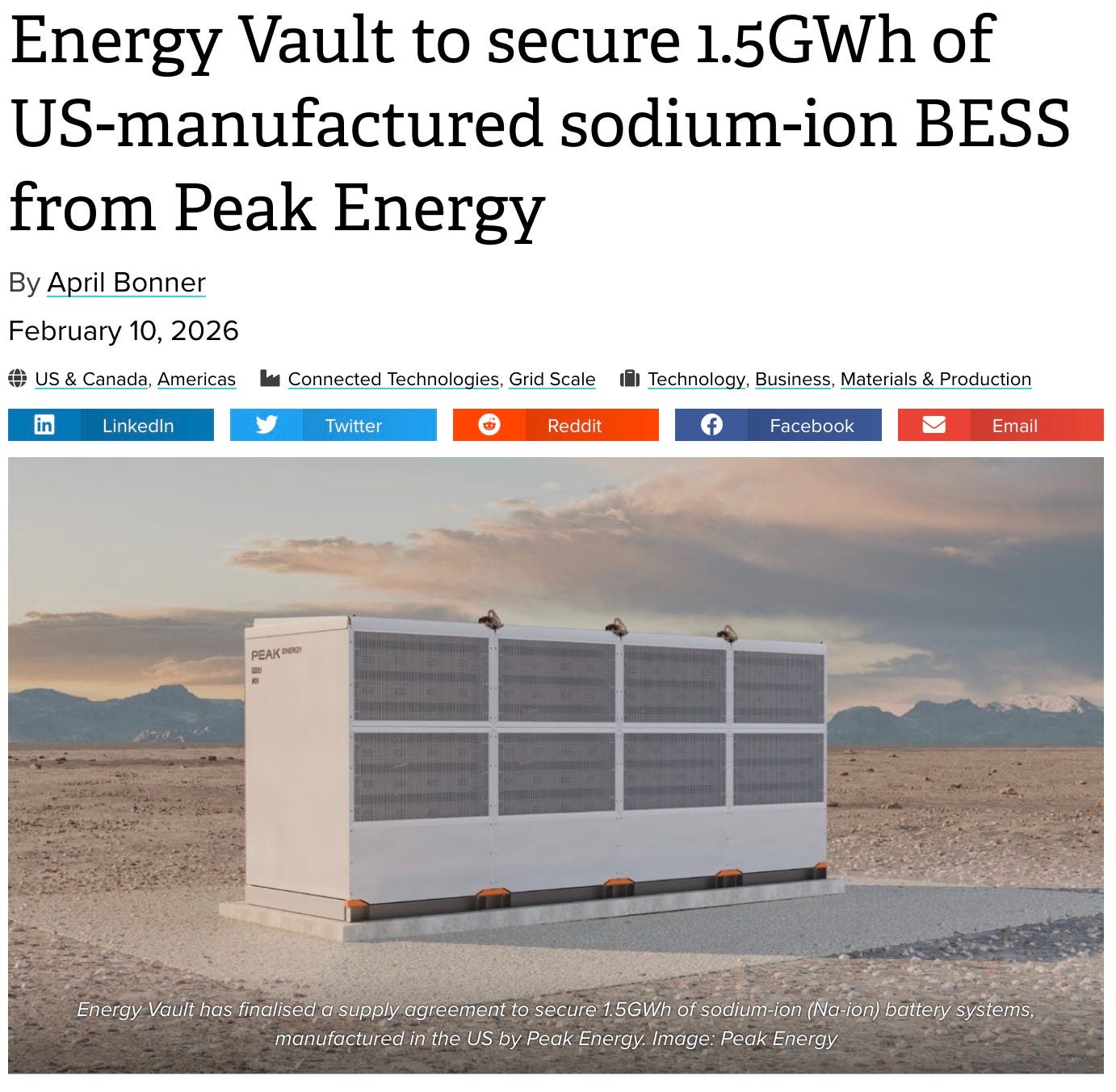

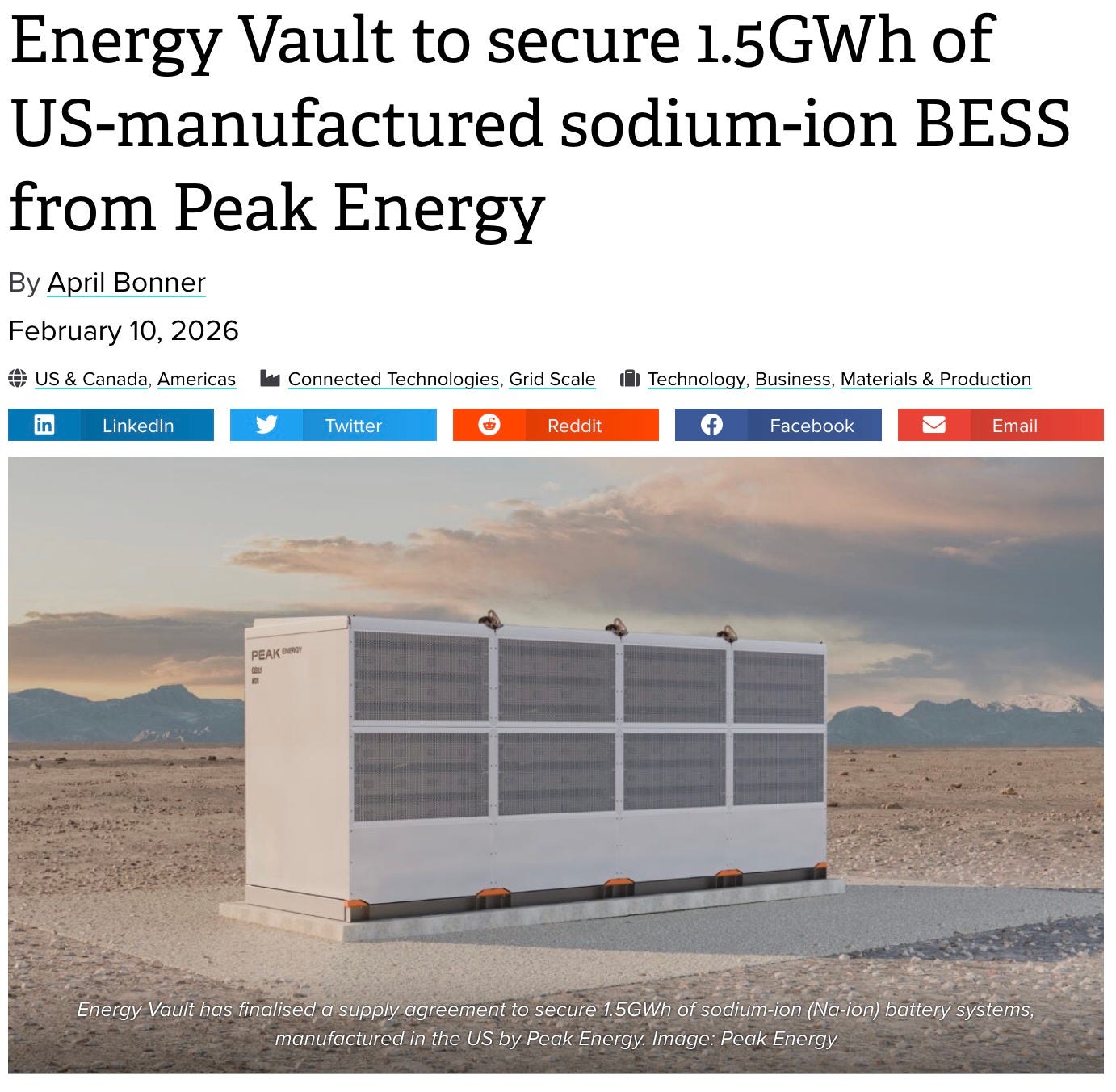

They are building AI data centre Battery infrastructure with Peak Energy (Bringing Sodium Ion Batteries to production in the west

Exclusive rights to bring Sodium Battteries from Peak in Japan and Australia

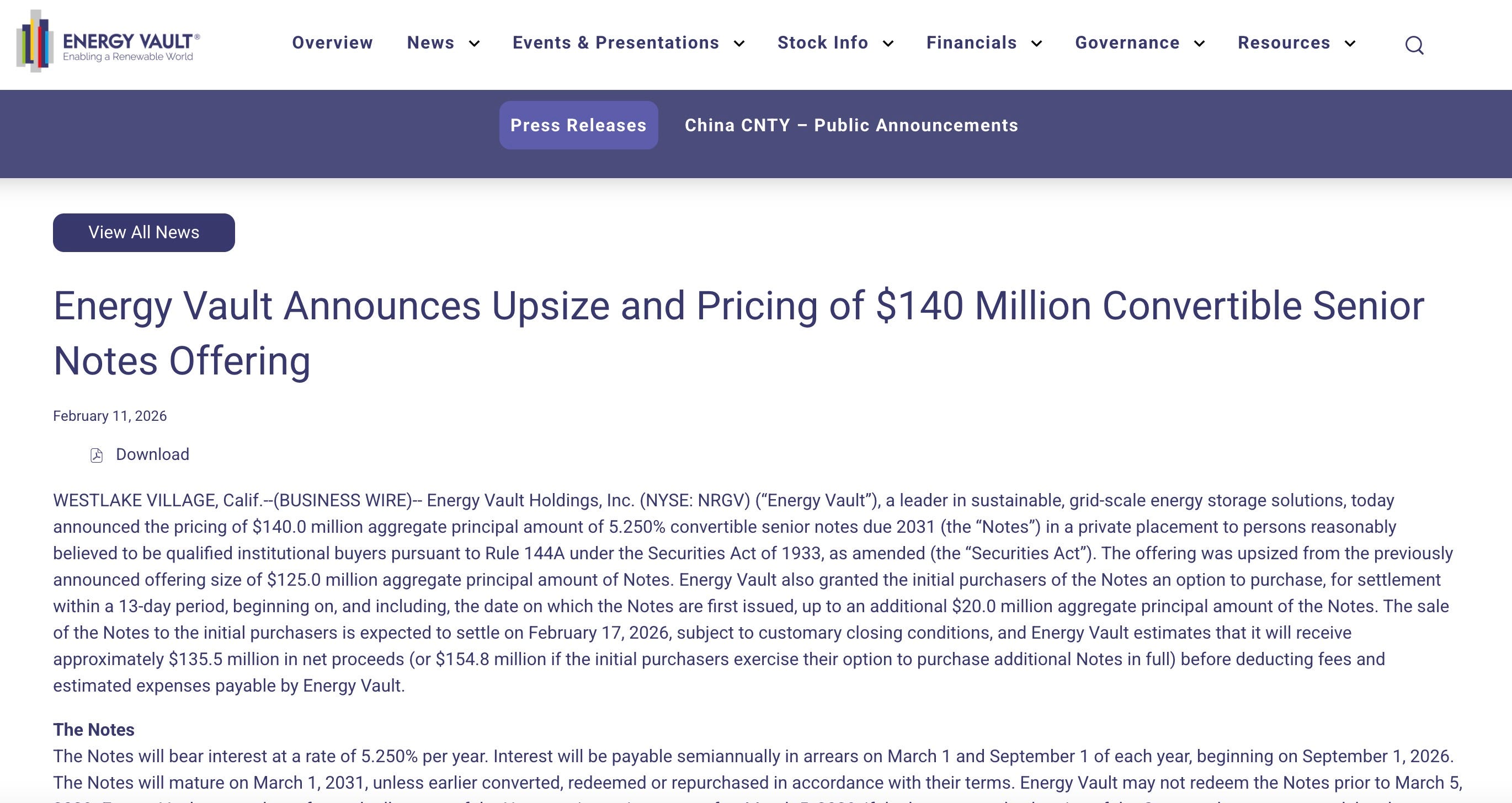

Private investors believe in it enough to raise 140M convertible

The deal was oversubscribed that why upsized from $125M to $140M

Not a dilution Fest.

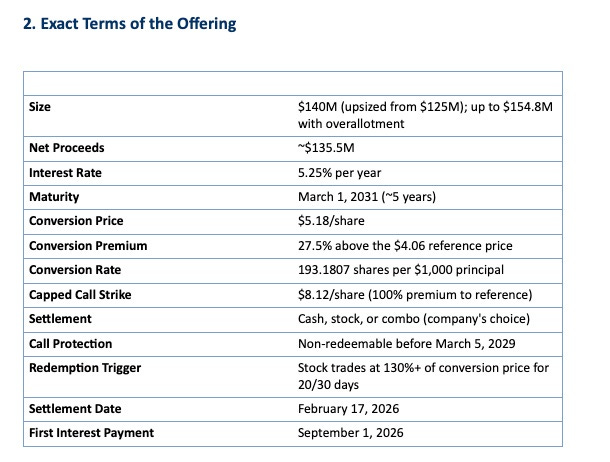

Lets unpack the Convertible debt terms here

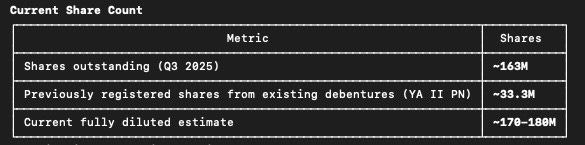

Lets look at fully diluted stocks

These are my estimates for the worst case dilution from this convertible debt raising.

The capped call is the critical detail. Here’s how dilution actually plays out at different stock prices:

Stock Price: Below $5.18

Dilution Impact: Zero dilution

What Happens: Notes stay as debt. No conversion. You just pay 5.25% interest.

────────────────────────────────────────

Stock Price: $5.18 to $8.12

Dilution Impact: Effectively zero dilution

What Happens: Notes are in-the-money BUT the capped call offsets the dilution. Company can settle in cash, stock, or combo.

────────────────────────────────────────

Stock Price: Above $8.12

Dilution Impact: Incremental dilution begins

What Happens: Only on the portion above $8.12. Example: at $10/share, dilution is only on the $10 - $8.12 = $1.88 spread per share, not the full

conversion.

────────────────────────────────────────

Stock Price: Way above $8.12 (e.g., $15+)

Dilution Impact: Full ~27M share dilution

What Happens: But at that point, the stock has nearly 4x’d — dilution is a “good problem to have.”

Key insight: If the stock stays between $4 and $8.12, there is essentially NO dilution from these notes. The dilution only matters if the stock

rips past $8.12, and at that point shareholders have already made 100%+ gains.

I created a thread from the last earnings call. Wanted to get this article out before market open. As I build more conviction on this name, I will share my deep dives into their tech.

DO NOT GO IN WITH SIZING. It’s Only a spec position for me

1/8 Energy Vault (NRGV) pivoted from pure EPC to asset owner, and Q3 shows the Asset Vault story getting real.

Asset Vault platform formally launched this quarter

First two Texas and California storage IPP assets now operating

Strategy targets top-quartile returns at “privileged” interconnect points

2/8 Management frames Q3 2025 as “one of the most pivotal” in company history, with execution catching up to strategy.

Four projects now operating or in construction totaling 340 MW

These initial assets expected to deliver >40 M EBITDA annually

10–15 year contracted revenue tails as projects come online

3/8 The OIC preferred deal now funds a sizable self-reinforcing growth engine where NRGV builds, owns, and services its own assets.

300 M preferred equity from OIC closes, launching Asset Vault Fund 1

Fund 1 enables >1.1 B CapEx across 1.5 GW storage projects

NRGV expects 100–150 M cash flow back from project margins and services

4/8 Asset origination is ramping fast, with NRGV leaning into both grid storage and emerging AI power demand.

Acquired 150 MW SOSA interconnect site near Houston from Savion

Stoney Creek 125 MW project in Australia backed by 14-year offtake

Collaboration deepening with Crusoe on AI data center power solutions

5/8 Commercial momentum is visible in backlog and pipeline, even with tariff noise and macro uncertainty in the U.S. market.

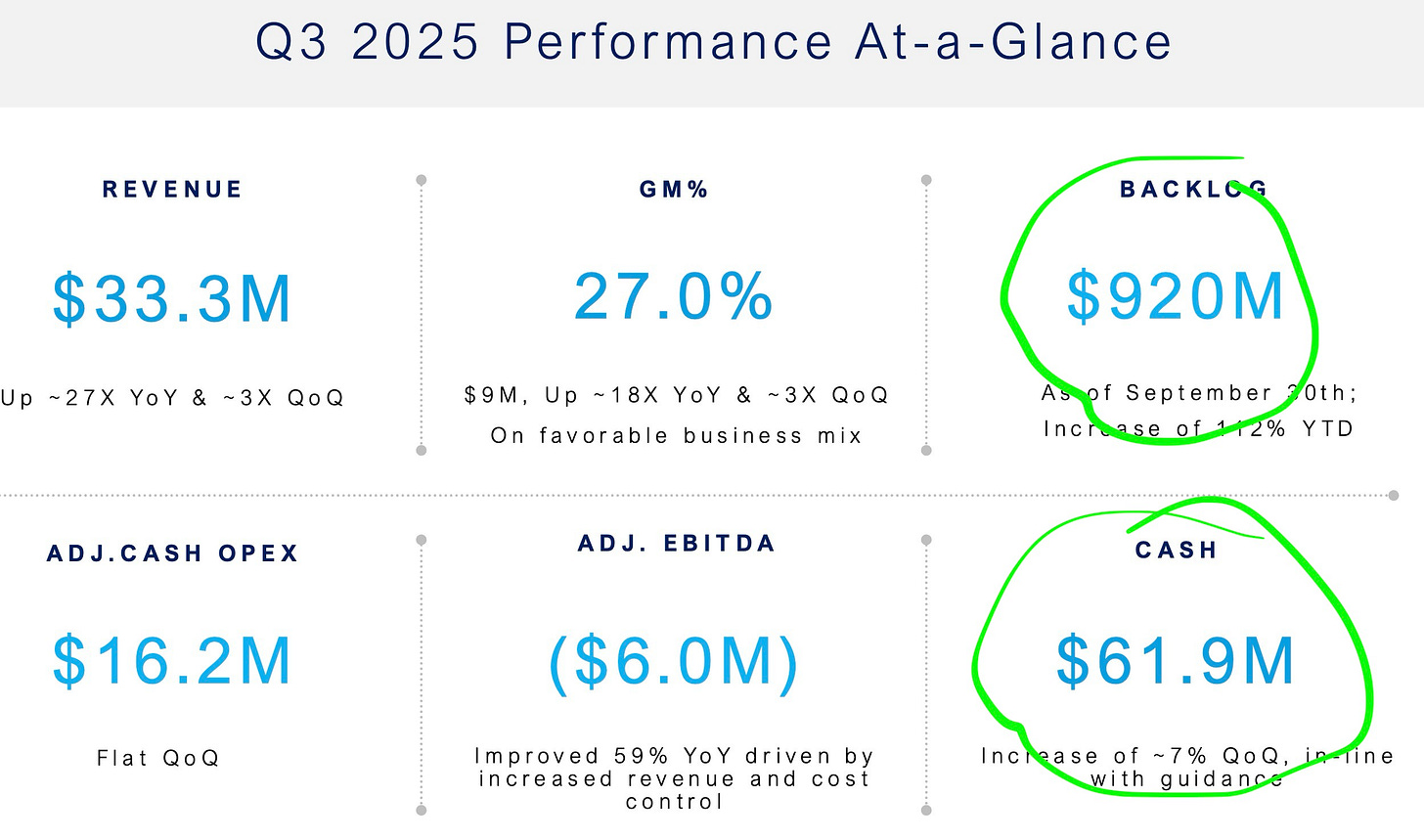

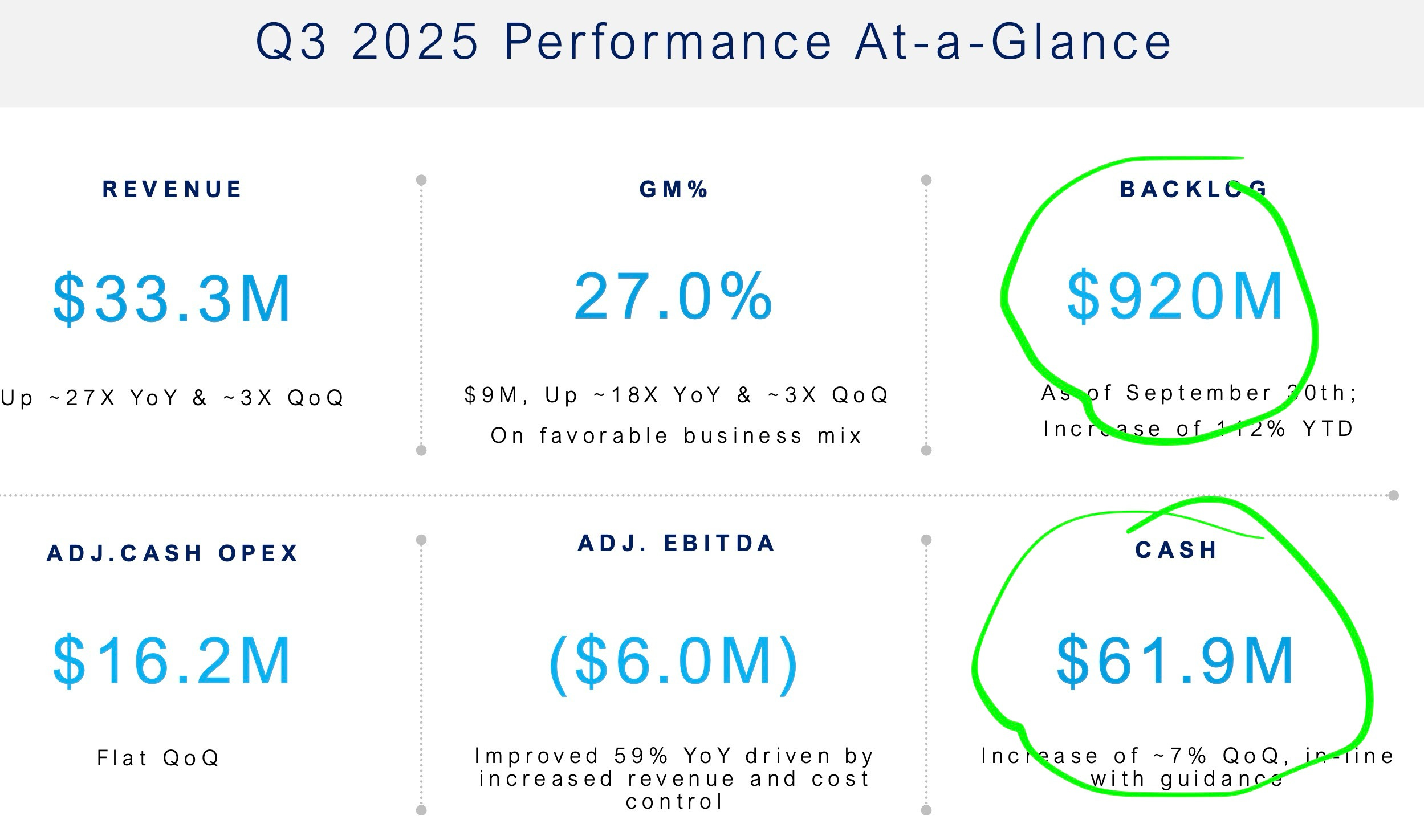

Revenue backlog at 920 M, up 112% year-to-date

Backlog has more than 4x’d since Q3 2024

Development pipeline sits around 2.1 B, or 8.7 GWh advanced projects

6/8 On the call, management stressed diversification and agility as buffers against U.S. tariffs and policy volatility.

Only about 10% of backlog exposed to U.S. tariff swings

Australia represented more than half of Q3 revenue

Asset Vault pipeline curated for “upper-tier” IRR and bankable offtake

7/8 Financially, Q3 shows the early earnings power of the new model, even on a small revenue base.

Q3 revenue 33.3 M vs 1.2 M a year ago, up ~27x

Q3 gross margin 27%, year-to-date gross margin ~32.6%

Adjusted EBITDA loss narrows to 6 M from 14.7 M loss last year