Fact checking Serenity and my DD on Valens Semiconductor ($VLN)

VLN semi for Autonomous cars and Robotics

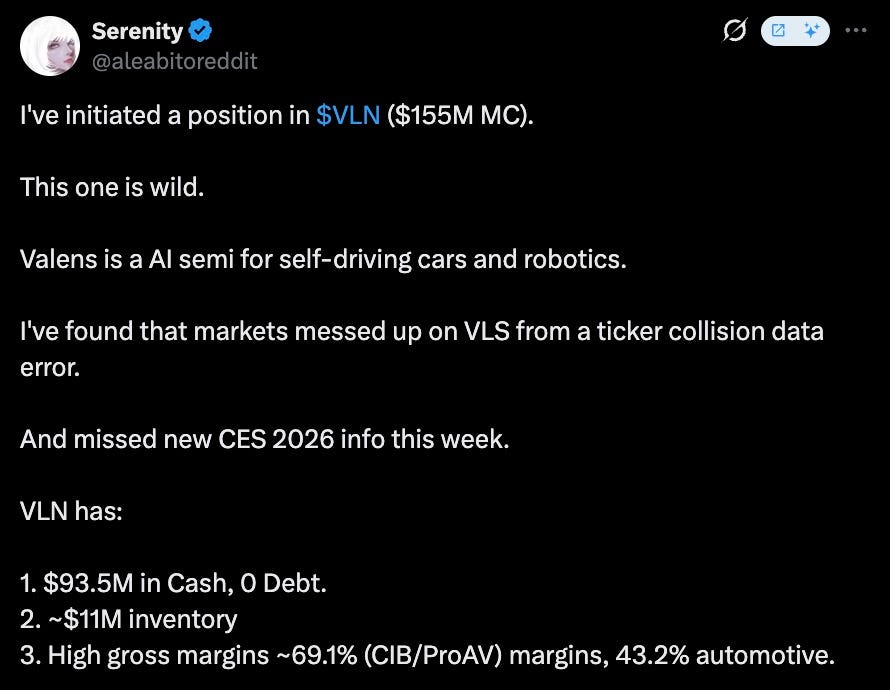

On 9th of Jan, Serenity (An insanely good X account) posted this

Serenity has been going viral in 2026 with some posts getting millions of impressions. This account is super respectable

So I had to check out and validate their claims

Debt is low. No crazy dilution. Ofcourse lossmaking. But the revenues is steady since a few quarter. All right, interesting, lets dive deeper.

It’s an Israeli company so they are not required to file 10Q. But I found the relevant file quickly. I fact checked claims and formed opinion about the company in this article

You all know how deep in fundamentals I like to get

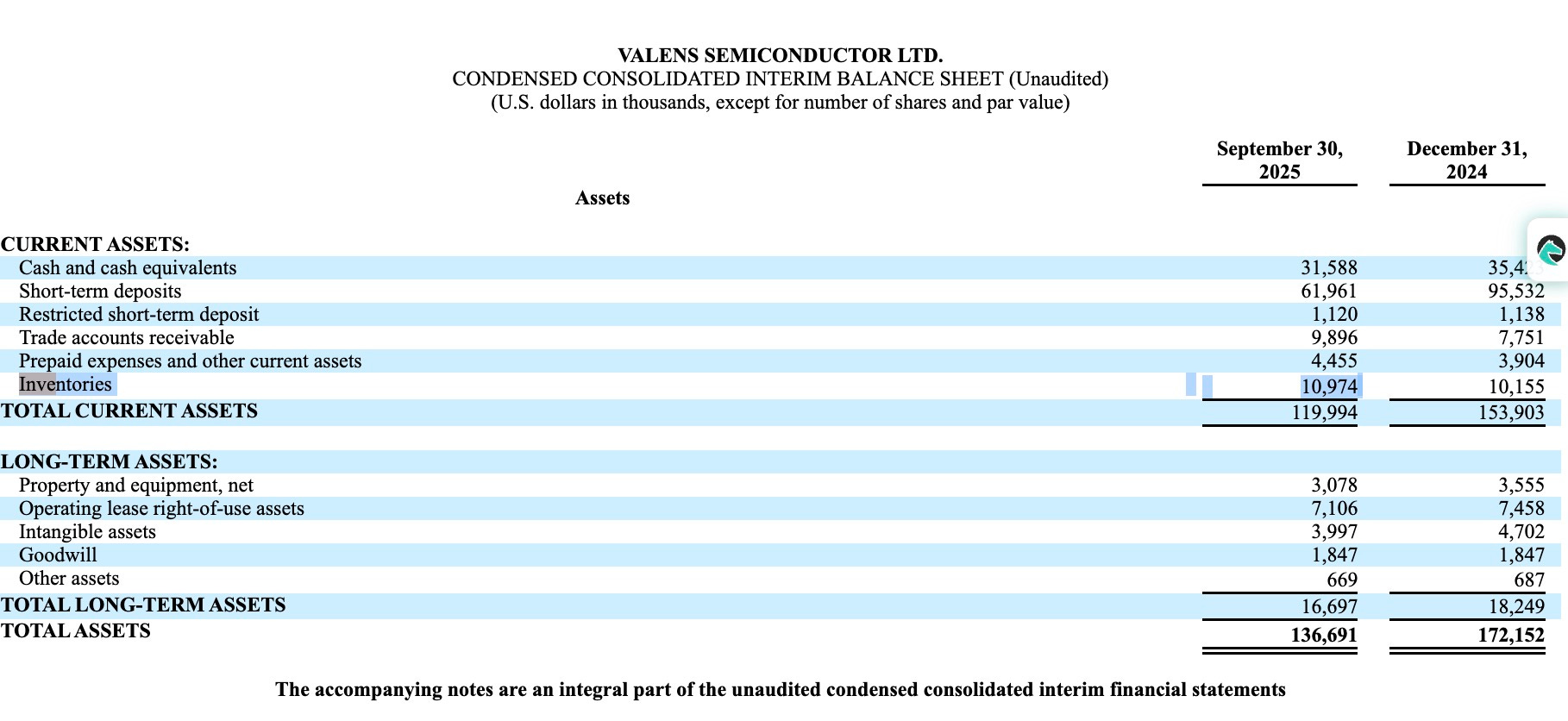

The inventories claim actually check out. It is indeed only $10.9M. Lets fact check all important claims

1. Claim: “$93.5M in Cash, 0 Debt.”

Verdict: TRUE.

Evidence: The Balance Sheet shows Cash and cash equivalents ($31,588) + Short-term deposits ($61,961) = $93,549 (thousands).

Debt: There is no line item for “Long-term debt” or “Bank loans.” The only liabilities are trade payables, accrued compensation, and lease liabilities (which are operational, not interest-bearing debt in the traditional sense)

2. Claim: “~$11M inventory.”

Verdict: TRUE.

Evidence: The Balance Sheet lists Inventories at $10,974 (thousands).

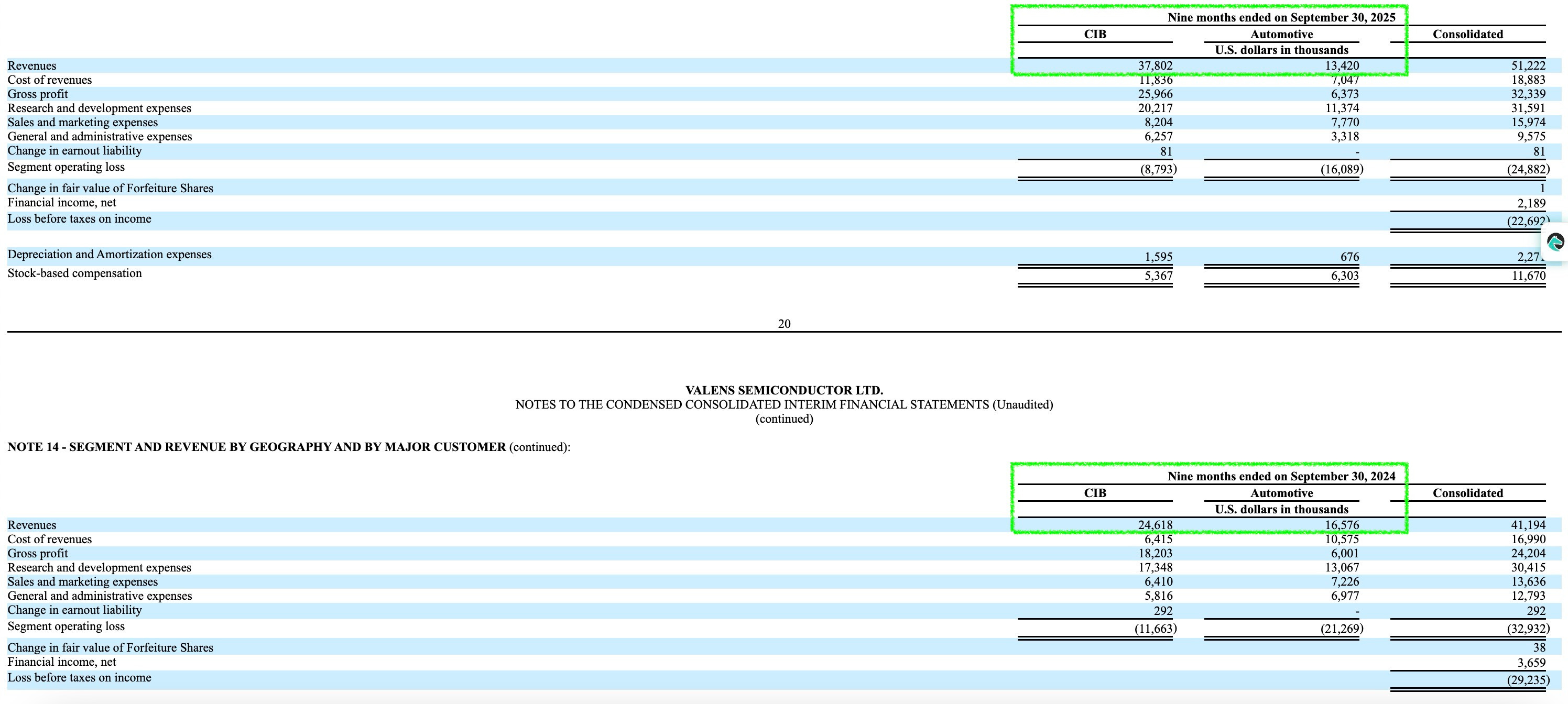

3. Claim: “High gross margins ~69.1% (CIB/ProAV) margins, 43.2% automotive.”

Verdict: MOSTLY TRUE (Automotive is actually higher).

Evidence: Note 14 (Segment Info) for 9 months ended Sept 30, 2025:

CIB: Gross Profit $25,966 / Revenue $37,802 = 68.7% (Very close to 69.1%).

Automotive: Gross Profit $6,373 / Revenue $13,420 = 47.5%.

Note: The tweet actually understates the Automotive margins (43.2% vs actual 47.5%), perhaps relying on Q3 specific data (which was 43.2%), but the 9-month trend is strong.

4. Claim: “Inventory of US$82 million... is a typo.”

Verdict: TRUE (The math supports the typo theory).

Evidence: Total Assets are $136,691 (thousands).

Cash/Deposits: ~$93,549.

Remaining assets allowed: $136,691 - $93,549 = $43,142.

It is mathematically impossible for the company to have $82M in inventory because $93M (Cash) + $82M (Inventory) = $175M, which exceeds the Total Assets reported ($136M). The inventory is definitively ~$11M.

5. Claim: “New CES 2026 info... pivot to robotics.”

Verdict: TRUE

Evidence: The acquisition of Acroname (described in Note 3 as “specializing in advanced automation and control technologies”) and the massive growth in the CIB segment (which includes machine vision/industrial) financially supports the narrative that they are pivoting to robotics.

6. Claim: “Extremely heavy dilution at $11.5 Strike from warrants.”

Verdict: TRUE.

Evidence: Note 12 lists “Private Warrants: 3,330,000” and “Public Warrants: 5,750,000” that were excluded from EPS calculations because they are anti-dilutive (meaning the stock price is currently below the strike price). While the filing doesn’t explicitly list the “$11.50” strike price in the text, this is the standard SPAC warrant strike price, and the presence of ~9M warrants is confirmed in the notes.

Following are some of my insights on the company that might help you decide if you want to jump in with Serenity

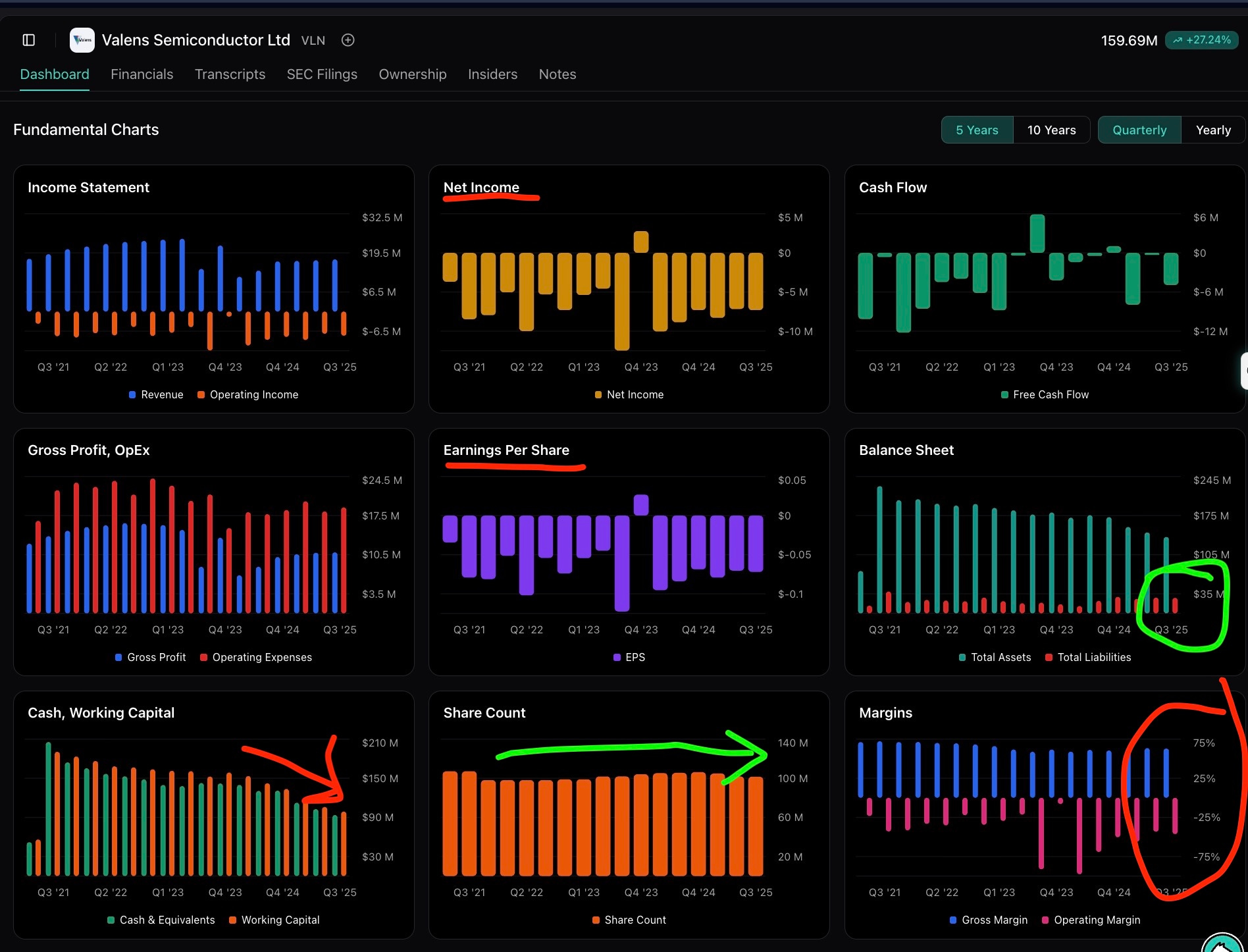

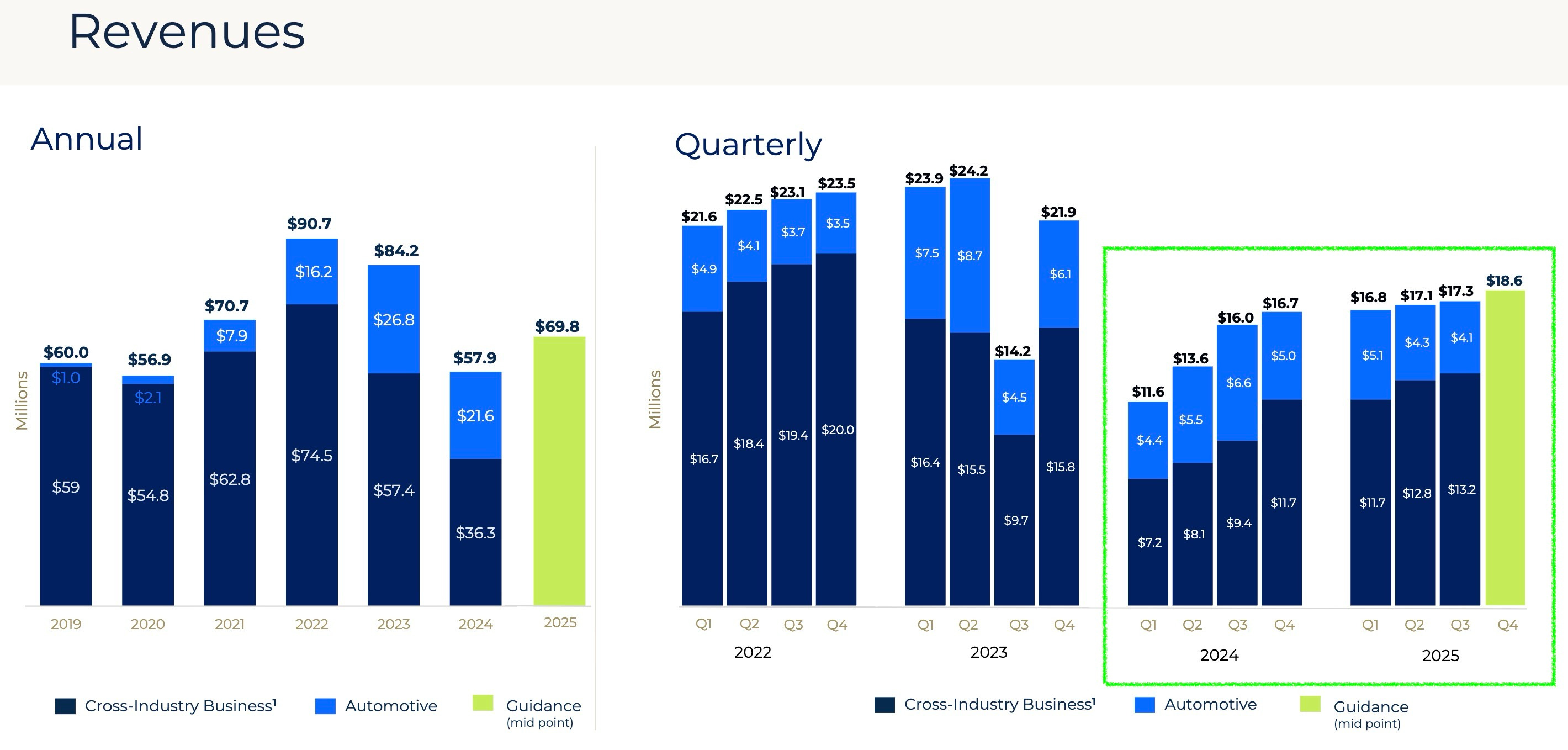

1. The “Growth” Story is Lopsided (Automotive is actually shrinking)

While the company is often pitched as an Automotive AI play, the filing reveals that Automotive revenue actually declined year-over-year for the 9-month period (from $16.6M in 2024 to $13.4M in 2025). The entire revenue growth of the company is currently being driven by the Cross Industry Business (CIB) segment, which grew back ~53% ($24.6M to $37.8M).

Could this be the start of CIB recovery? I love the thesis that Robotics play will be able to be validated quickly (~6 months)

2. Aggressive Buybacks Despite Operating Losses

It is highly unintuitive for a company reporting a Net Loss of $(22.8M) to spend more cash on share repurchases ($23.4M) than it lost in operations. Usually, loss-making growth companies hoard cash. Valens is aggressively returning capital to shareholders, behaving more like a mature cash-cow than a loss-making semi growth stock.

3. The “Acroname” Acquisition Masked Organic Burn

The acquisition of Acroname (Note 3) added ~$4.1M in revenue for the 9-month period. Without this acquisition, the company’s revenue growth would look less impressive. Furthermore, the acquisition brought in $1.3M in cash, slightly padding the cash flow statement against the purchase price.

4. Inventory Composition Shift (Finished Goods vs. WIP)

While total inventory rose slightly ($10.1M to $10.9M), the mix shifted drastically. Work in Process (WIP) dropped by ~21%, while Finished Goods spiked by ~32%. This suggests the company has converted raw materials into sellable chips but hasn’t shipped them yet. This could indicate either preparation for a big order or a sudden slowdown in demand where production outpaced sales

5. Acroname might be hitting ambitious targets

The company has a liability of ~$2.5M for “Earnout” payments to Acroname shareholders (Note 8). The fair value of this liability increased (an expense of $81k), which unintuitively is a “good” sign—it implies the acquired company (Acroname) is likely hitting the performance targets required to trigger those payments.

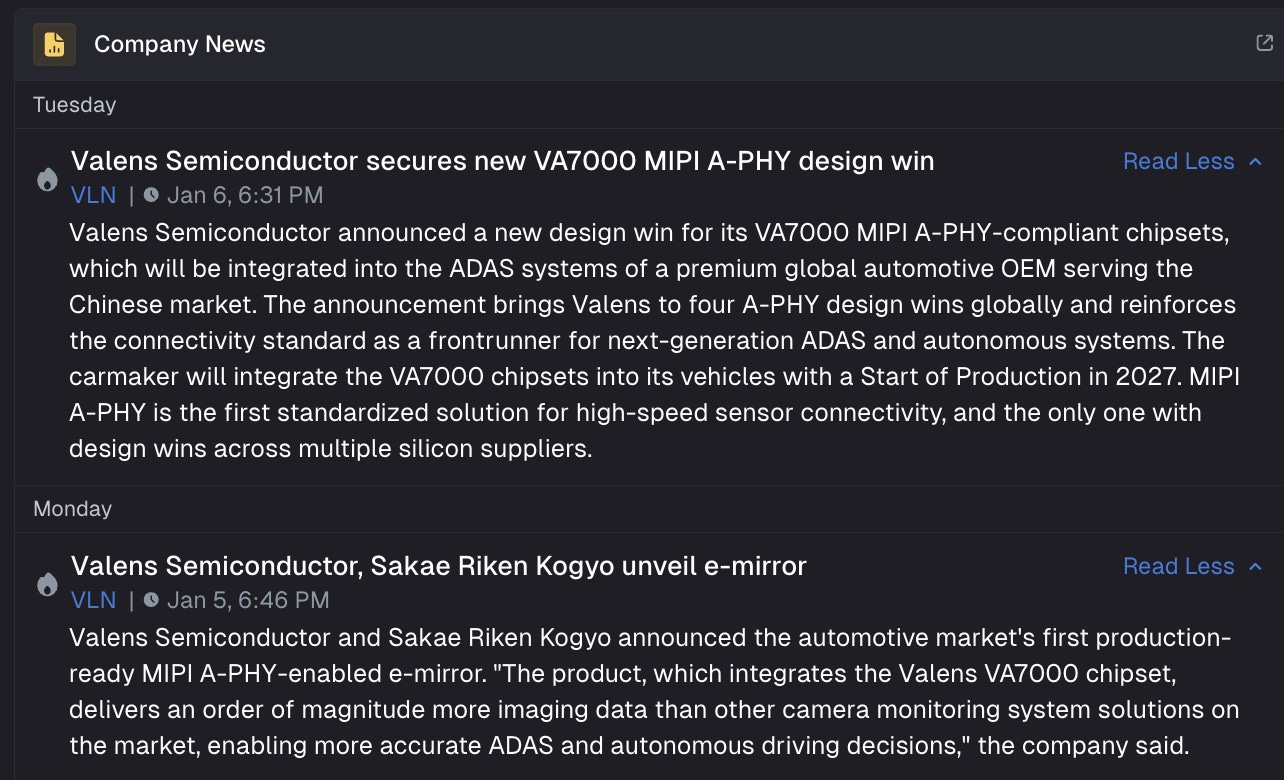

They filed important design wins in 2026

This a great long-term opportunity and it is definitely real, but near-term catalysts for technical products and growth remain 12-18 months away.

7. Subsequent Event: CEO Change Signals Pivot

There is a new CEO appointed in Nov 2025. Combined with the shrinking Automotive revenue and the massive options grant (4M options) to the new CEO, this suggests the Board was dissatisfied with the previous trajectory. It validates the “pivot” narrative

MY VERDICT

This is indeed mispriced and might still be substantially cheap after a 50% move on Friday. Fair value seems to put the stock price at $4-7. I am keeping this in my watchlist. As for the future of the product it requires more due diligence

RISKS

One of the risks not mentioned in his post, is that there is considerable Insider sales. CEO has been periodically selling,

Founder Ex CEO Dror has sold about 10% of his holdings in the last month (Total only 1% of the outstanding shares). Maybe it’s not such a bad thing since he stepped down as CEO in Nov 2025

2. One-Time “Insurance” Profit Boosted Q3

In Q3 2025, the General and Administrative (G&A) expenses were unusually low ($2.2M vs $5.8M in Q3 2024). Note 5 reveals this was due to an insurance recovery asset of $1.476M recognized regarding a customer claim. This is a non-recurring event that artificially made the Q3 operating loss look significantly better than it actually was operationally

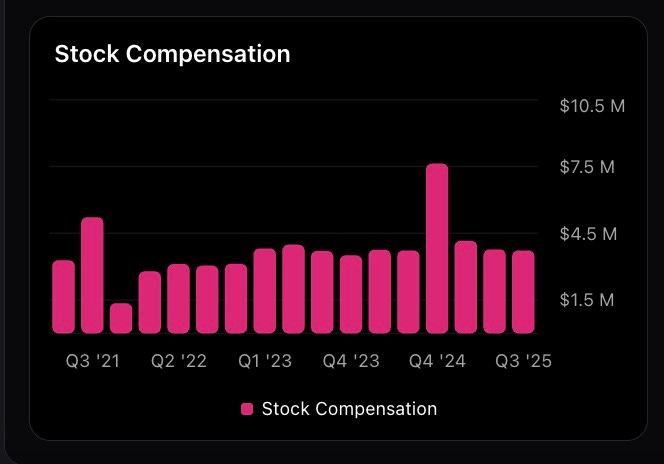

High Stock-Based Compensation (SBC) Relative to Revenue

The company incurred $11.7M in stock-based compensation on $51.2M in revenue (9 months). This means ~23 cents of every dollar of revenue is effectively paid out in equity to employees. While this preserves cash, it is a significant dilution driver that is excluded from “Adjusted EBITDA” metrics often used by analysts.